Let's deal with some basics. The default choice for all participants in my 401a is the Balanced Pooled

Fund (B/P Fund). This fund is a combination of the Met Life GIC and American Funds, PIMCO, and Vanguard bond funds, in

the majority (60%) for a lot of stability, and a mix of stock funds in the minority (40%) for some horsepower. Think

of it as the worst of both worlds for many 401a participants, especially the youngest and the oldest. When stocks are

hot, you are not. Your 401 is more bonds than stocks and bonds tend to lag when stocks are hot. When stocks do

go down, you still have a substantial position in them. See the B/P Funds/McMorgan's 2000-2003 performance. When

bonds go up, they don't go up much. If they do go up a lot, it's A VERY BAD THING.

Been there, done that in the 80's. The Tshirt said,

The Unemployment Rate Is 12%,

Car Loans Cost 18%. MM Funds Pay 18%,

And

Double Tax Free Muni's Pay 12%.

This Is Not A Happy

Time For Many Americans.

When bonds go down, they don't

go down much...unless something comes seriously unglued. Two Heartland Advisors Muni Bond Funds lost about 50% of their

value overnight...it's not like it can't happen. And yes, I do mean overnight. On the morning of October

13th 2000, the holders of the two funds had balances worth 69% and 44% less than what they held the previous day.

(http://www.businessweek.com/2000/00_50/b3711203.htm) But mostly with bonds you pretty much always get the principle back and steady, if

pretty unimpressive income along the way. Hopefully you make more in return than you lose to inflation. But

if the bond fund has to sell bonds when demand is slack in order to meet redemptions or rebalance the portfolio, you

lose money in what is supposed to be the safest investment available. You lose principal and the fund

risks having to buy lower yielding paper in the future. Whatever. If I had $50,000,000, it'd be

different. It just wouldn't matter if I didn't keep up with inflation. I'd own lots of bonds, 'cuz

it would take a long time to put a dent in $50 Mil. But I don't. So I want substantial exposure to bonds

only under certain specific circumstances. If I was comfortably retired, near the end of my life, and I had more

than enough money to last, and I valued my ease and relaxation more than anything else, again, it'd be different.

But I'm still working and I'm not willing to risk running short of income later in life when I'm least able

to do anything about it. I don't intend to become a burden to my childen. So again, I want substantial

exposure to bonds only under certain specific circumstances.

In summary, the Balanced Pooled Fund gives you offsetting positions in stocks and bonds. Supposedly, when stocks

go up, bonds go down and visa versa. It's like betting on both the black and red at the roulette table. You

win one and lose one on each spin. The house takes both bets if 0 or 00 show, but that's not often, so

it's like a small fee for playing. Now think of the Balanced Pooled Fund. You divide your money into two parts and each part works

against the other part and some of it goes away in fees. Make sense to you? Me neither.

Since I'm digging my 401a defined contribution plan out of a hole generated by

the prior Balanced Pooled Fund, I'm looking for a positive rate of return ex inflation. I simply

can't afford to lose any more money in the name of a good safe solid quality investment and I can't push retirement

out another 10 years in the name of the appearance of safety. I've generally got no use for the Balanced Pooled Fund

because it promotes very mediocre returns and a false sense of security.

The Balanced Pooled Fund is great if ;

You don't care to be bothered. Doing nothing and relying on other people to do what's best for you is always

the right thing to do.

You been burned too badly before by McMorgan's Aggressive Allocation

model to accept anything but hunkering down and freezing up.

You don't care what

your pension income is. You figure you'll probably get by just fine with a little adjustment.

You'll just cut back on your lifestyle a little more each year and every time prices go up...

You've always viewed having more money to spend as a major problem. No money, no problem. Be happy.

You don't know or care what opportunity cost is.

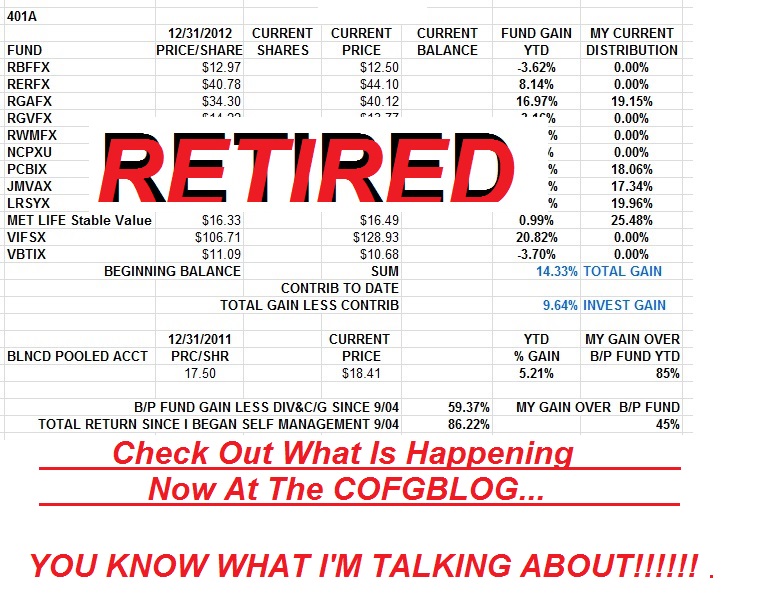

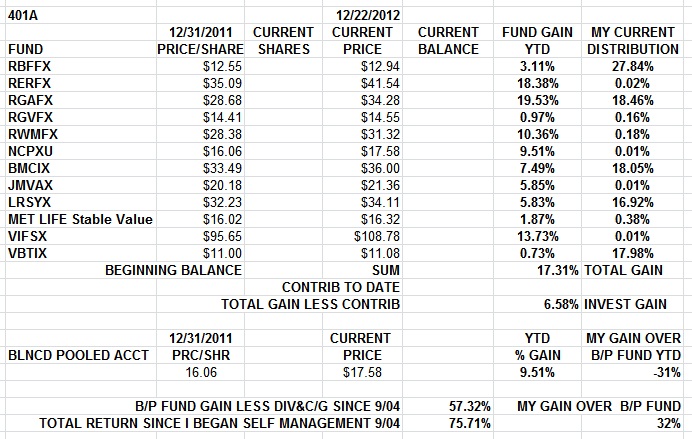

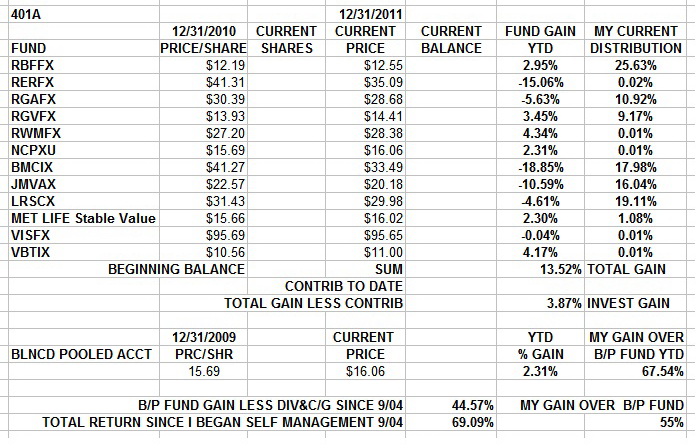

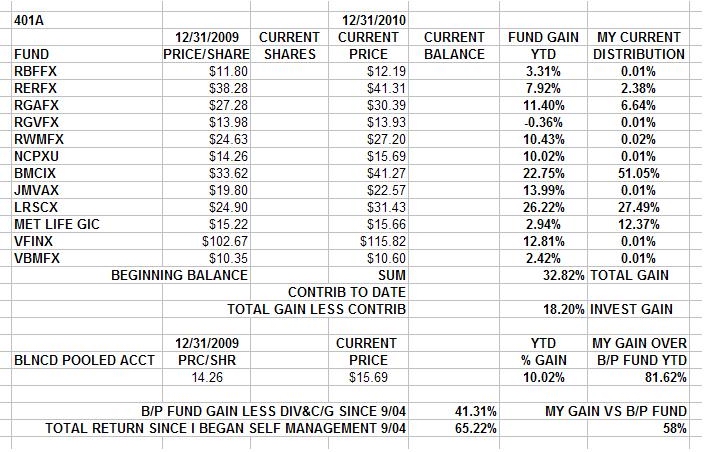

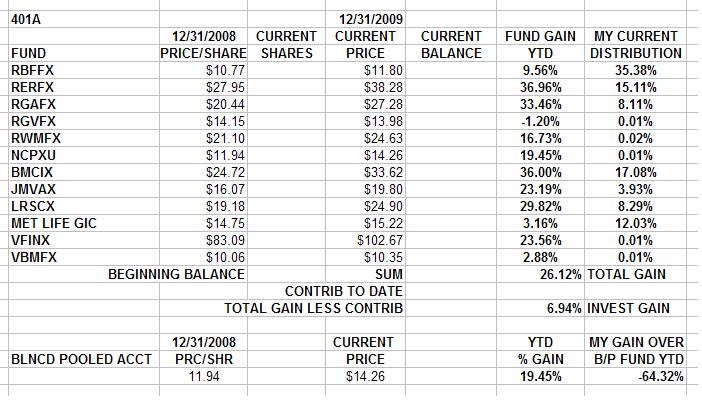

Check out this web site's chart page, my blog, and my personal account tables for relative returns to see what I mean about the B/P Fund's return.

I'm willing to look for more return at the cost of higher risk and

I'm willing to offset the risk by putting an hour or two of work a week into the management of my self

managed pension plan and I'll write about it too. Whatta deal. Read on....