I'd Like To Think I'm Starting To Get Traction On This 401a Thing. Talk To Me About It At The Next Meeting...

"The primary objective of leadership is to help those who are doing poorly to do well and to help those who are doing well to do even better."

-- Jim Rohn

Charts and Tables up.

The Conclusion of "My Most Gnarley Mutual Fund Adventure"

So, to sum up my FPRAX/IDETX affair:

1) No game goes on forever. If you buy, you are almost guaranteed to have to/want to sell given time. It was 12 years for FPRAX and 12 months for IDETX for me. When the game is over, you need to leave the table and go somewhere else or lose what you've gained.

2) It's the manager, not the fund. Or it's the era, not the fund. Or the economy. Or the world economy. Or national politics. Or world politics. Or whatever. Good funds can be totally wrong at any given time for a number of reasons. When things change, you change. Or pay the price.

3) Price and trend are what's important to you. Every day something happens somewhere that can meaningfully affect your investment. Often it can, but it doesn't. Price and trend will always tell you what is really going on. It's the only unequivocal, direct, and elemental information that you can get. Unfortunately, it is about the past and not the future. No one said that this was easy.

3) You need to direct a self directed plan and you need information to do that. Given that there are pro's in place at the funds applying their knowlege, experience, and judgement on your behalf, you still are making a decision every day or every week or every month as to whether or not they will continue to do so. Is what they are doing working? Go back to the chart pages on my web site if you have any doubt that YOU CAN NOT AFFORD NOT TO KNOW THAT ANSWER. There's always something you need to know. You need to learn how to get the information and apply it. Get used to it.

4) No one cares about your money the way you do. The investment industry cares that your money shows up and stays so that it generates the fees to pay their salary. The legal authorities care that laws about managing your money are not broken. There is no law that says it is illegal for you to lose your money in bad investments or for fees and piss poor management to fritter away your future. The market doesn't care about your money, your hopes, or your dreams. It doesn't care about anything, whatsoever, period. You are the only one who REALLY cares about your hard earned money and the return it should earn you. And only you will make the hard choices that need to be made when the time comes. Do you really expect a money manager to fire himself because making you money or stopping you from losing money is more important than him keeping his job?

5) It's not a sin to be wrong. That's why there are erasers and whiteout openly for sale and not behind the counter. I screw up, the President screws up, surgeons and street sweepers screw up, everybody screws up. It IS a sin to STAY wrong. It cost Bill Sams his job and FPRAX and IDETX my money. That's why McMorgan no longer is our only pension fund advisor. Don't let the possibility of being wrong paralyze you. But the idea of being wrong and staying wrong should cause you to break out in a cold sweat. When I look back at the McMorgan era, I do...

6) The investment industry will tell you to stay fully invested at all times; you might miss a money making opportunity and cost them some fees if you don't. Notice how nothing is ever said about missing out on falling into a crater and not losing most of your investment by not being fully invested when it all turns to shit? That would cost the money managers some fees. Besides, you probably may most likely do OK or even well in the long run if you stay long and are lucky and things work out and anyway, they get their fees that way. And besides, they can't charge you fees and take your money if you don't stay the course. It's all about the fees, see... Of course if you look at the charts for FPRAX and IDETX, you'll see that during certain times, having the money in cash in a coffee can or in a money market fund was brilliant investing at its best compared to buy and hold investing. More about this later.

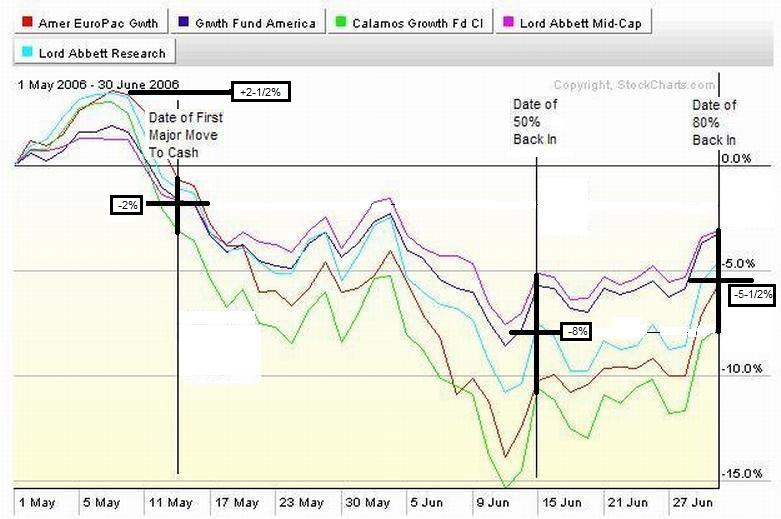

The chart is live. CLICKONNIT

The chart shows my moves into cash and back into stocks since May 1st. I declared victory a coupla months early in March and went partially to cash and it cost me a little in missed performance. Or not. I really don't know or care. It was not worth tallying up. I declared victory three days too late in May and it cost me substantially; a quarter of my return since 9/04 went away in four days time before I went to mostly cash. But I caught most of the move right and I protected 75% of my profits earned since 9/04. I booked a 30% profit in under two years and smoked what I'da done by staying in the B/P Fund. By the middle of May, the market coulda dropped like a stone and I'd have had it mostly covered. By June 9th, I was totally faded; I was pretty much all cash and maximally protected against losses. I was totally protected from profits on the way back up, but that's the way it goes.

As described below, on June 16th I went 50% back in. That worked out OK, and as of Friday afternoon, I'm 80% back in.

If you rub your eyeball on the chart above, you see that my moves 1) Bought me piece of mind during a brutal and bloody downdraft that had the pro's bleeding from the gums. The drop was very ugly in terms of the rate of fall and the lack of any respite on the way down. The lack of any short term bounce made it a very unusual occurrance. And I was in cash for almost all of it. 2) It made me a dollar, too. If you postulate that I was equally represented in each fund, then you can estimate that the midpoint of each heavy vertical bars on the chart represents my positions. It looks like I sold most of my positions at about 5% down from the peak in early May and about 2% in the hole in terms of the price as of the 1st of May. It also looks like I bought back half the positions at about 6% below that. It looks like I spent most of the remaining cash getting back in at 3-1/2% below where I sold. Just as an eyeball guess, I'd say that by selling when things got hairy and buying back when things looked better, that I'd bought not only peace of mind and safety in the case of a severe and prolonged crash, but made back some of the money I'd left on the table by not bailing out earlier. Far out.

See ya at the Hall. We gotta vote on the contract and money allocation if we pass on it. And of course we've gotta move on a special called meeting on the pension plans.... My motion to do so is still outstanding and it's time to firm the meeting up.

[ view entry ] ( 1063 views ) [ 0 trackbacks ] permalink -- Jim Rohn

Charts and Tables up.

The Conclusion of "My Most Gnarley Mutual Fund Adventure"

So, to sum up my FPRAX/IDETX affair:

1) No game goes on forever. If you buy, you are almost guaranteed to have to/want to sell given time. It was 12 years for FPRAX and 12 months for IDETX for me. When the game is over, you need to leave the table and go somewhere else or lose what you've gained.

2) It's the manager, not the fund. Or it's the era, not the fund. Or the economy. Or the world economy. Or national politics. Or world politics. Or whatever. Good funds can be totally wrong at any given time for a number of reasons. When things change, you change. Or pay the price.

3) Price and trend are what's important to you. Every day something happens somewhere that can meaningfully affect your investment. Often it can, but it doesn't. Price and trend will always tell you what is really going on. It's the only unequivocal, direct, and elemental information that you can get. Unfortunately, it is about the past and not the future. No one said that this was easy.

3) You need to direct a self directed plan and you need information to do that. Given that there are pro's in place at the funds applying their knowlege, experience, and judgement on your behalf, you still are making a decision every day or every week or every month as to whether or not they will continue to do so. Is what they are doing working? Go back to the chart pages on my web site if you have any doubt that YOU CAN NOT AFFORD NOT TO KNOW THAT ANSWER. There's always something you need to know. You need to learn how to get the information and apply it. Get used to it.

4) No one cares about your money the way you do. The investment industry cares that your money shows up and stays so that it generates the fees to pay their salary. The legal authorities care that laws about managing your money are not broken. There is no law that says it is illegal for you to lose your money in bad investments or for fees and piss poor management to fritter away your future. The market doesn't care about your money, your hopes, or your dreams. It doesn't care about anything, whatsoever, period. You are the only one who REALLY cares about your hard earned money and the return it should earn you. And only you will make the hard choices that need to be made when the time comes. Do you really expect a money manager to fire himself because making you money or stopping you from losing money is more important than him keeping his job?

5) It's not a sin to be wrong. That's why there are erasers and whiteout openly for sale and not behind the counter. I screw up, the President screws up, surgeons and street sweepers screw up, everybody screws up. It IS a sin to STAY wrong. It cost Bill Sams his job and FPRAX and IDETX my money. That's why McMorgan no longer is our only pension fund advisor. Don't let the possibility of being wrong paralyze you. But the idea of being wrong and staying wrong should cause you to break out in a cold sweat. When I look back at the McMorgan era, I do...

6) The investment industry will tell you to stay fully invested at all times; you might miss a money making opportunity and cost them some fees if you don't. Notice how nothing is ever said about missing out on falling into a crater and not losing most of your investment by not being fully invested when it all turns to shit? That would cost the money managers some fees. Besides, you probably may most likely do OK or even well in the long run if you stay long and are lucky and things work out and anyway, they get their fees that way. And besides, they can't charge you fees and take your money if you don't stay the course. It's all about the fees, see... Of course if you look at the charts for FPRAX and IDETX, you'll see that during certain times, having the money in cash in a coffee can or in a money market fund was brilliant investing at its best compared to buy and hold investing. More about this later.

The chart is live. CLICKONNIT

;)

The chart shows my moves into cash and back into stocks since May 1st. I declared victory a coupla months early in March and went partially to cash and it cost me a little in missed performance. Or not. I really don't know or care. It was not worth tallying up. I declared victory three days too late in May and it cost me substantially; a quarter of my return since 9/04 went away in four days time before I went to mostly cash. But I caught most of the move right and I protected 75% of my profits earned since 9/04. I booked a 30% profit in under two years and smoked what I'da done by staying in the B/P Fund. By the middle of May, the market coulda dropped like a stone and I'd have had it mostly covered. By June 9th, I was totally faded; I was pretty much all cash and maximally protected against losses. I was totally protected from profits on the way back up, but that's the way it goes.

As described below, on June 16th I went 50% back in. That worked out OK, and as of Friday afternoon, I'm 80% back in.

If you rub your eyeball on the chart above, you see that my moves 1) Bought me piece of mind during a brutal and bloody downdraft that had the pro's bleeding from the gums. The drop was very ugly in terms of the rate of fall and the lack of any respite on the way down. The lack of any short term bounce made it a very unusual occurrance. And I was in cash for almost all of it. 2) It made me a dollar, too. If you postulate that I was equally represented in each fund, then you can estimate that the midpoint of each heavy vertical bars on the chart represents my positions. It looks like I sold most of my positions at about 5% down from the peak in early May and about 2% in the hole in terms of the price as of the 1st of May. It also looks like I bought back half the positions at about 6% below that. It looks like I spent most of the remaining cash getting back in at 3-1/2% below where I sold. Just as an eyeball guess, I'd say that by selling when things got hairy and buying back when things looked better, that I'd bought not only peace of mind and safety in the case of a severe and prolonged crash, but made back some of the money I'd left on the table by not bailing out earlier. Far out.

See ya at the Hall. We gotta vote on the contract and money allocation if we pass on it. And of course we've gotta move on a special called meeting on the pension plans.... My motion to do so is still outstanding and it's time to firm the meeting up.

( 3 / 1574 )

( 3 / 1574 )

Calendar

Calendar