Im always thinking about losing money as opposed to making money. Dont focus on making money; focus on protecting what you have.

Paul Tudor Jones

Ahm jes' anudder ol' broked down retahrd union pipefitter.

I retired in September of 2013 after 40 years in the trade, five years after this picture was taken. At the time, there was only one retired pig inna picture. Now there would be two...

I had started actively managing my 401 in 2004, after leaving it untended and with the minimum contribution since its inception in 1991. I was too busy raising a family, building America, and riding, racing and writing about motorcycles to pay any attention to saving for retirement. After all I had my Defined Benefit Plan and an IRA or two. What more could I need? Big mistake. I had contributed the minimum amount to the Defined Contribution Plan and left the funds in the default Balanced Pooled Fund. But between 2000 to 2003, I had to straighten out a coupla my IRA's after the dotcom-9/11 financial crash had crushed them, and as an afterthought, I then applied the same kind of evaluation to my 401 account and to my defined benefit pension fund. I found both to be in desperate straights. I was able to help turn both around. The story of both my IRA's and 401 are in part on my website.

Once I was able to get decent returns from my 401, I increased my contributions until I was maxed out and started to save some serious coin and to make serious returns for my retirement. It worked out really well... So far.

I have a nice income from my defined benefit pension plan and Social Security. Today. But my pension plan has no cost of living adjustment.

"What Is Hip Today Might Become Passe'"

-- Tower Of Power

http://www.youtube.com/watch?v=SN8pWdZhVaM

http://www.youtube.com/watch?v=vauqRuvzVgs

Only 30% of my pension income, the Social Security part, adjusts for inflation. The continued wellbeing of my wife and I is dependent on how I handle my retirement savings.

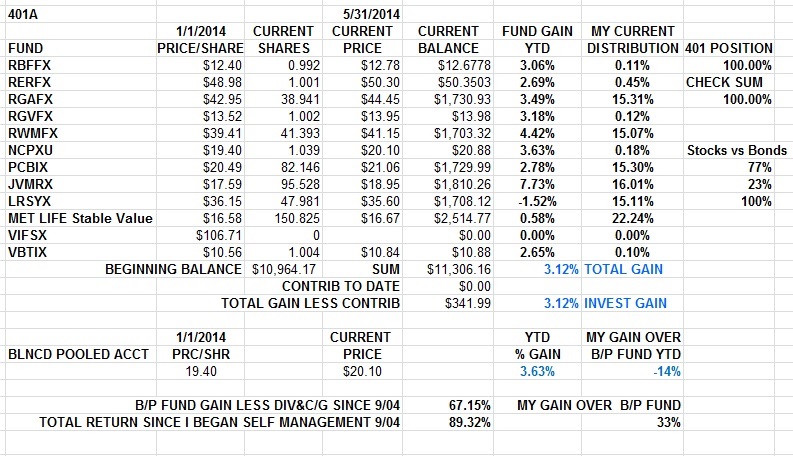

Since retirement, I've given almost all of my 401/IRA balance over to professionals. But not all. I've kept $10K in my Union 401 account to provide a benchmark for the professionals and to keep the 401 account open should I decide to take management of the funds back. Here's where I have the money allocated, how I've done this year and since I started managing my 401(table), and how I've done since I started managing my 401 post retirement in 2013 (chart).

Note that this is my personal 401 account, managed for and by me, as I see fit, for Where my head is at and my perceived needs. I have Social Security and a defined benefit pension for regular income and I am looking to generate serious returns on my retirement savings for future use when my fixed pension income falls seriously behind my cost of living inflated needs. I am aggressive in nature but with three generations (wife and I, kids, and grandkids) to think about, I gotta make the right moves. I can stand the volatility of this approach, the gains are proven, and it is a plan. It's my plan..

I've made a copy of the Excel spreadsheet I use to track and manage my 401 available to download on my website. If you are not in my Local, the spreadsheet can be adapted to other 401s and other mutual funds by someone with a modicum of Excel experience.

I post here what I read that I find of significance or interest. I allocate funds within the 401 between aggressive and conservative allocations as circumstance and inclination require based on what I read and some professional level subscription data. Running the blog keeps me honest with myself. Putting it in writing makes sure I really have a grip on the handle.

http://www.politico.com/magazine/story/ ... 4ow0PmICm4

In Fucking Credible... Grrrr.

http://www.washingtonpost.com/sf/nation ... -coverups/

Tuesday...

http://www.businessinsider.com/nra-stat ... ers-2014-6

Wednesday...

http://www.businessinsider.com/shake-sh ... ers-2014-6

http://www.businessinsider.com/when-the ... ded-2014-6

;)

-- Tower Of Power

;)

;)

http://pragcap.com/should-you-use-an-au ... nt-service

Thursday...

http://www.businessinsider.com/preet-bh ... ent-2014-6

http://www.nytimes.com/2014/06/04/opini ... .html?_r=0

( 2.9 / 1654 )

( 2.9 / 1654 )

Calendar

Calendar