Even Republican pundits acknowledge that they are likely to lose the House this year. If the Demo's can't win this year, When can they? And if they can't, do we need to reexamine our political alliances? Appended 4/5

Thoughtless risks are destructive, of course, but perhaps even more wasteful is thoughtless caution, which prompts inaction and promotes failure to seize opportunity.

-- Gary Ryan Blair

It's a new month, so there are new Fundalarm.com tables. More about that below. There are also new charts and personal account data tables. (More about that too...) I stood pat last week; I'd gone from 90%/10% stocks and bonds/cash to 70%/30% three weeks ago. Discipline, ya know; Yin/Yang, cycles, Buy/Sell, what goes around comes around, that kinda stuff. I gotta keep my sellin' muscles limbered up; If I am going to go where there is money to be made, I gotta be ready to go away from where there is money to be lost. That said, I'm thinkin' that I'm gonna bleed some cash back to equities. I'm at a new all time high for return (35% since 9/03) and the way I play the game is to go where the action is and stay until the party is over. If I could always call the exact top and bottom, you wouldn't be reading this. So I want to make enough to still have a good return even if I'm late leaving this party and late arriving at the next one. And since 9/03 I HAVE made enough. Go with what got you there until it doesn't work. I'm gonna. More about THAT below...

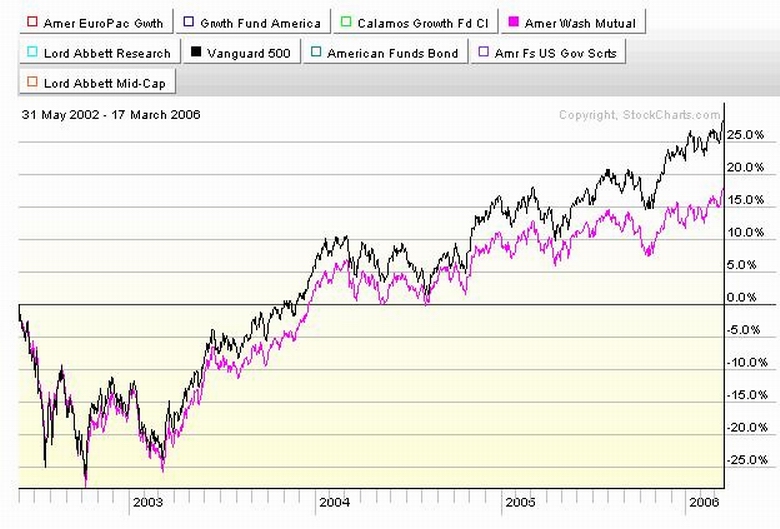

Speaking of thoughtless caution, I went to the 401 meeting a coupla weeks ago with a buddy who I'm mother-henning through the process. I ended up in a shouting match w/ Mike M. over some things. One of them is the Washington Mutual fund which we have in the 401. Check out the chart below;

CLICK ON IT, IT'S LIVE!

The Fundalarm data tables call RWMFX a Two Alarm fund. I say it's on its way to a three alarmer. It looks and performs like an S&P500 fund only not as well. An S&P500 fund is a nonmanaged fund that represents the market as a whole. We get that currently with the VFINX fund at a VERY low management fee. I don't see paying a higher fee to mirror the Vanguard fund but make less money. Mike M. does. He defended it based on 50 years of good performance and meeting the approval of the PE Teachers of Washington DC retirement association or some other group that I failed to make a note of, based on not recapitulating the crash of '29. Or so I remember. What he said didn't make much sense. If the management team that was in place for the last 50 years is still there, they're really old and I'm not surprised that they aren't doing well. If they are not still in place, why quote what the fund did a lifetime ago with different managers? I can't retire on historical performance, nor relative performance and neither can you.

But what really ticked me off was this; Mike spent 45 minutes on identity theft. Granted this is important and very much today. He then crammed the 401 material into half an hour because he promised someone an early out. Then he gave out wrong information on the threshold for market timing in the various funds and suggested looking at the 401 account once year. Here's why this pissed me off. Check out the chart below.

CLICK ON IT, IT'S LIVE!

This chart shows all the funds available to us. Note that we've lost money being in the bond funds. Less than even after 2-1/2 years? Gimme a break. No reason to be there and I'm not. That's not a safe return, that's bleeding assets. Note also that the Washington Mutual Fund is the worst fund that doesn't lose money. I still think we were sold that fund for a spiff, as part of the American Fund package, or just name recognition. No reason to be there either, and I'm not (kinda). Finally, note the performance of the Balanced Pooled Fund (B/P Fund) that I've penciled in (electrophotonically speaking). I've got an ugly suspicion that the B/P Fund is mostly the bond funds and the WashMu, with a little bit of some funds that are doing well. It sure looks that way. I think I'm in WAMU whether I like it or not and I KNOW I'm stuck in bonds to the extent that I'm in the B/P Fund. Ask Mike M. about it...

Here's the big issue for me; I met a buddy at the KJ memorial who works in the next local south. He's retiring next year after 27 years and with $3100 a month to show for it. I know of an individual in the next local west who has 20 years down and $4.5K/month to show for it. The sparky I work next to has 20 years down and $3k/month to show for it. I have a 30 year pin and about $2100/month to show for it. Can I retire successfully on 1/3rd to 2/3 of what other workers in neighboring locals do? Looks like I'll find out. And so will the other members of my local.

The 401 is going to be vital in me being able to retire successfully. I've worked hard to get a decent 401 plan into place starting in the fall of 02 because every member including me is going to rely on it more than we ever imagined. That's what is most important to the members of my local, not identity theft. If Mike's tired of giving the same old 401 lecture, I'll need to see that it is no longer needed before I'll back off. And as long as my local's members have a less than adequate defined benefit plan and are thoughtlessly cautious in being in the BP Fund, I'll be there. Show me that the members of the local are knowlegable about and resigned to uncertain and poor future and I'll back off. As for not looking at the 401 but once a year, you see the results of THAT kind of thinking elsewhere on this website. That kinda crap is what got our previous plan advisor bounced out and Mike M. in. As for not knowing the current fund's policies on market timing,....

This month's contribution came in and I put that money and some of the GIC money where the getting is good; the RERFX fund and the LRSCX fund. I'm still makin' money, I'm 14% cash, I'm still one day away from the complete safety of 90% cash if and when, and I've personally confirmed that it is possible to sell as well as buy without the world coming to an end. The personal account data table has been updated to reflect the situation deliniated above. Se ya at the hall...

-- Gary Ryan Blair

It's a new month, so there are new Fundalarm.com tables. More about that below. There are also new charts and personal account data tables. (More about that too...) I stood pat last week; I'd gone from 90%/10% stocks and bonds/cash to 70%/30% three weeks ago. Discipline, ya know; Yin/Yang, cycles, Buy/Sell, what goes around comes around, that kinda stuff. I gotta keep my sellin' muscles limbered up; If I am going to go where there is money to be made, I gotta be ready to go away from where there is money to be lost. That said, I'm thinkin' that I'm gonna bleed some cash back to equities. I'm at a new all time high for return (35% since 9/03) and the way I play the game is to go where the action is and stay until the party is over. If I could always call the exact top and bottom, you wouldn't be reading this. So I want to make enough to still have a good return even if I'm late leaving this party and late arriving at the next one. And since 9/03 I HAVE made enough. Go with what got you there until it doesn't work. I'm gonna. More about THAT below...

Speaking of thoughtless caution, I went to the 401 meeting a coupla weeks ago with a buddy who I'm mother-henning through the process. I ended up in a shouting match w/ Mike M. over some things. One of them is the Washington Mutual fund which we have in the 401. Check out the chart below;

CLICK ON IT, IT'S LIVE!

;)

The Fundalarm data tables call RWMFX a Two Alarm fund. I say it's on its way to a three alarmer. It looks and performs like an S&P500 fund only not as well. An S&P500 fund is a nonmanaged fund that represents the market as a whole. We get that currently with the VFINX fund at a VERY low management fee. I don't see paying a higher fee to mirror the Vanguard fund but make less money. Mike M. does. He defended it based on 50 years of good performance and meeting the approval of the PE Teachers of Washington DC retirement association or some other group that I failed to make a note of, based on not recapitulating the crash of '29. Or so I remember. What he said didn't make much sense. If the management team that was in place for the last 50 years is still there, they're really old and I'm not surprised that they aren't doing well. If they are not still in place, why quote what the fund did a lifetime ago with different managers? I can't retire on historical performance, nor relative performance and neither can you.

But what really ticked me off was this; Mike spent 45 minutes on identity theft. Granted this is important and very much today. He then crammed the 401 material into half an hour because he promised someone an early out. Then he gave out wrong information on the threshold for market timing in the various funds and suggested looking at the 401 account once year. Here's why this pissed me off. Check out the chart below.

CLICK ON IT, IT'S LIVE!

;)

This chart shows all the funds available to us. Note that we've lost money being in the bond funds. Less than even after 2-1/2 years? Gimme a break. No reason to be there and I'm not. That's not a safe return, that's bleeding assets. Note also that the Washington Mutual Fund is the worst fund that doesn't lose money. I still think we were sold that fund for a spiff, as part of the American Fund package, or just name recognition. No reason to be there either, and I'm not (kinda). Finally, note the performance of the Balanced Pooled Fund (B/P Fund) that I've penciled in (electrophotonically speaking). I've got an ugly suspicion that the B/P Fund is mostly the bond funds and the WashMu, with a little bit of some funds that are doing well. It sure looks that way. I think I'm in WAMU whether I like it or not and I KNOW I'm stuck in bonds to the extent that I'm in the B/P Fund. Ask Mike M. about it...

Here's the big issue for me; I met a buddy at the KJ memorial who works in the next local south. He's retiring next year after 27 years and with $3100 a month to show for it. I know of an individual in the next local west who has 20 years down and $4.5K/month to show for it. The sparky I work next to has 20 years down and $3k/month to show for it. I have a 30 year pin and about $2100/month to show for it. Can I retire successfully on 1/3rd to 2/3 of what other workers in neighboring locals do? Looks like I'll find out. And so will the other members of my local.

The 401 is going to be vital in me being able to retire successfully. I've worked hard to get a decent 401 plan into place starting in the fall of 02 because every member including me is going to rely on it more than we ever imagined. That's what is most important to the members of my local, not identity theft. If Mike's tired of giving the same old 401 lecture, I'll need to see that it is no longer needed before I'll back off. And as long as my local's members have a less than adequate defined benefit plan and are thoughtlessly cautious in being in the BP Fund, I'll be there. Show me that the members of the local are knowlegable about and resigned to uncertain and poor future and I'll back off. As for not looking at the 401 but once a year, you see the results of THAT kind of thinking elsewhere on this website. That kinda crap is what got our previous plan advisor bounced out and Mike M. in. As for not knowing the current fund's policies on market timing,....

This month's contribution came in and I put that money and some of the GIC money where the getting is good; the RERFX fund and the LRSCX fund. I'm still makin' money, I'm 14% cash, I'm still one day away from the complete safety of 90% cash if and when, and I've personally confirmed that it is possible to sell as well as buy without the world coming to an end. The personal account data table has been updated to reflect the situation deliniated above. Se ya at the hall...

Calendar

Calendar