The 1971 version of the Allman Bros Band...The sound board tapes from the F'mo East and West are incendiary. You owe it to yourself....

"The market is not a sofa, it is not a place to get comfortable."

Jim Cramer

Chartz and Table Zup on www.joefacer.com....

I've been pretty much reporting on what's happening lately. Lots of charts, links, and a table or two. My strategy of riding the market up and standing aside when the market cracked has been pretty successful. It was loaded and cocked back in late '07 and other than trying to pick up pennies in front of a steamroller with small positions until mid June, I was heavily in cash at the end of the first quarter. Charts and tables on my website tell the tale. It is AMAZING how well being cautious has worked out. Risk control is HUGE in a self directed plan.

But Now What? That's EASY!!!

HOW I MANAGE MY 401A

Check out the charts on my site. www.joefacer.com We had a huge earning opportunity from 9/04 until 10/07. During those three years the worst stock fund in the 401a made 11% a year and the best fund returned 30% a year. Since 11/07, all of them except the American Funds Government Securities Fund and the Met Life GIC have gone into the toilet. The economy and financial markets run in cycles. The overall direction is up. But there are pitfalls to be avoided along the way. No shit. So I want to be in the market when the direction is up and out when the direction is down. Furthermore, I want to be in the right places in the market. I'll take what the market gives. Will things be as good as the last time? Doesn't matter. Ya gotta play what yer dealt. we'll see....

What about "Buy And Hold". Is "Buy And Hold" dead?

"Buy And Hold" died for me in 1998. See http://joefacer.com/id18.html for how and why. If you have 40+ years before retirement and in blind faith don't wish to make the effort regardless of the risks , it may still be alive for you. Whatever.

What about "You Can't Time The Market."

That's just dumb. You look at the run up from '98 to '01 and the run up from '03 to '07 and read the papers (the thoughtful articles, not the cheerleaders) and you can't recognize the top? You can't recognize a time to be REALLY cautious? A buddy at work went all cash in December of this year at my recommendation. Earlier, he and his wife had looked at a house they wanted and got all the way to getting qualified for the loan. He looked at the loan and figured the payments were 80% of his take home pay and he walked away. "You Don't Need A Weatherman To See Which Way The Wind Blows." Shit like that ALWAYS goes bad at some point.

Wall Street earns money off your investments. They can't justify fees on cash. They will ALWAYS tell you to "Stay The Course." Furthermore, the big money funds are $100's or $1000's of millions of dollars. They can't turn on a dime. Buy and hold is what it looks like even when they are bailing as fast as they can. I used to be able to turn on a dime. The McMorgan era was so gawdawful that I never contributed over the minimum. I didn't put much in and McMorgan didn't earn me much. When we got the new funds, I could spread my money around a little and get in and out of the market in three days. Now I'm contributing the max and have made a lot on my investments in the 401a. Now it takes some thought, but all the way in and all the way out takes about a week or so at the minimum to about a month at the maximum. If the cat walks on the keyboard and I gotta unscramble the account from some horrible gawdawful allocation, the fix takes a coupla days to get in gear and a week to a month to undo, regardless. No biggie. THIS is what it means to be "In It For The Long Run". If you sell when you shouldn't have, BUY IT BACK! Held on a little too long? Sell it late. Was it a mistake? Fix it! Being wrong by being too cautious or too aggressive for a week or a month is meaningless in the long run. It is not a sin being wrong, positioned either too risky or too safely. Everybody makes mistakes. The sin is to stay wrong long enough to dig yourself a hole you'll never get out of...

So there are two things to be dealt with sometime in the future.

When Is The Right Time To Get Back In? And Where Do I Go?

Well, GM, Ford and Chrysler warn that they see themselves crashing into bankruptcy and taking the economy with them by the end of 2008/2009 GM/Ford Chrysler. So they want the US taxpayer to make $50 to $100 Billion dollars available to them to see if that helps them work things out. AIG has spent the original $85 billion of taxpayer money and is starting in on an additional $36 billion and either wants more or a change of terms so that they are eligible to borrow more. That is only two of the many major problems we face now and in the near future. This looks like it will take time for things to work out if they do work out at all. So I've got plenty of time to look for when to get in and time to write about where to get in.

....In The Meantime...Here

Smokin' synopsis of the election....

http://www.newsweek.com/id/167582

http://www.ritholtz.com/blog/2008/11/fa ... democrats/

Prescient

http://www.theonion.com/content/node/28784

http://www.theonion.com/content/node/89486

http://www.ritholtz.com/blog/2008/11/me ... year-high/

http://www.ritholtz.com/blog/2008/11/un ... eremployed

http://www.ritholtz.com/blog/2008/11/no ... ober-2008/

http://www.ritholtz.com/blog/2008/11/th ... s-is-over/

http://www.ritholtz.com/blog/2008/11/ha ... residency/

http://www.ritholtz.com/blog/2008/11/do ... reclosure/

http://www.ritholtz.com/blog/2008/11/re ... fter-bush/

http://www.ritholtz.com/blog/2008/11/th ... -of-times/

http://www.ritholtz.com/blog/2008/11/ai ... ore-money/

http://www.ritholtz.com/blog/2008/11/th ... -of-palin/

http://www.ritholtz.com/blog/2008/11/th ... untaintop/

http://www.pbs.org/moyers/journal/11072008/watch.html

http://www.ritholtz.com/blog/2008/11/fo ... ng-hitler/

http://www.dailymail.co.uk/news/worldne ... -tale.html

See ya here later this weekend...

LIKE NOW!!!

CLICK THESE IMAGES...

CLICKIT

You know how I feel about bonds if you read this... http://joefacer.com/id11.html . Enuf said. Check out the chart above if that AIN'T enuf. It shows the two bond funds available to the 401a. Ordinarily you'd invest in these bond funds for safety. Check out the charts on my site's chart pages for what the cost of safety was for investing in bonds between 2003 and late 2007. Your performance sucked. Look at the cost of safety after 9/21/2007. It either blew you out of the water or you did OK. Let's see why...

CLICKLIT!!!!

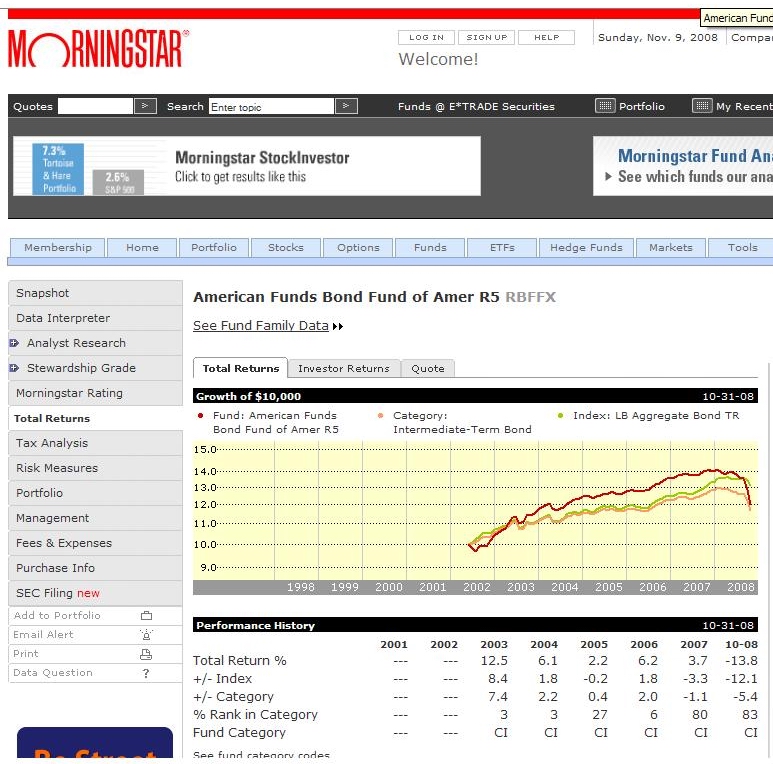

The first image is from MORNINGSTAR for which I have a link up above. It shows part of the RETURNS page for the RBFFX bond fund. The data shows that the fund did really well between 2003 and 2006 compared to the Lehman Bros Index and the category of similar bond funds. However returns in 2005 and 2007 were not as good. Returns in '08 have been disastrous. It is still kind of a respectable showing for a short time period. It is a respectable showing in terms of the category and in terms of realizing not as much gain in return for safety and low investor effort. Still if the safety is not there, especially if the market changes, then you can't make a real serious case for being in the fund even if you didn't want to go through the effort and risk of doing better with stocks. The RGVEX government bond fund and the MET LIFE GIC offered competitive returns in bonds or a cash like fund year over year and maybe more safety. We'll have to look at them next week.

CLICKIT!!!

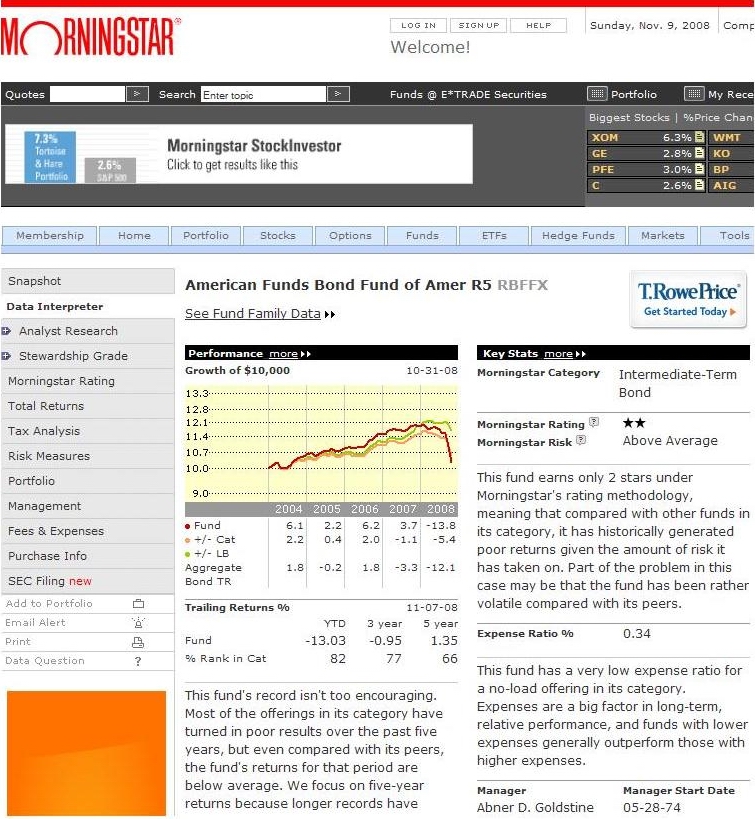

Above is the MORNINGSTAR DATA INTERPRETER page for the RBFFX Fund. Morningstar looks at the fund from a different view point and puts on its analyst hat. Morningstar is not impressed. Rather than looking at the returns in individual years, it lumps the years together and looks at trailing returns versus other funds. The bad '07 and '08 returns ripped the guts out of the total picture. The safety was not there. The fund had 26% of it's (your) money in mortgages and 48% of the money in corporate bonds. When these sectors went down in flames so did the safety and your money. Returns were low and the risk was high. The worst of both worlds. Add in the "unusual securities" and "structured notes which are basically bonds" (HORSE EXHAUST) and this fund looks like trouble.

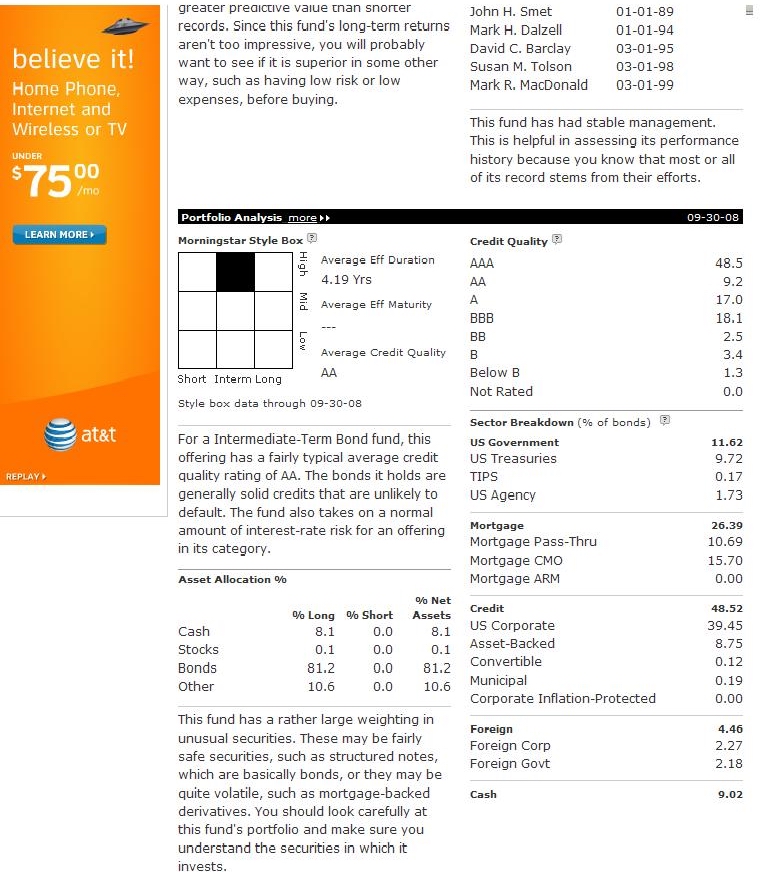

The bottom line is TANSTAAFL. There Ain't No Such Thing As A Free Lunch. The word bonds does NOT mean safe and you can never look away from your money or it may go away. When things were good, I never saw the returns from this fund being good enough to make me want to put money in. There were stock funds and the GIC and RGVEX bond fund. Once things went bad, there was too much risk and big losses and only the thinnest illusion of safety in RBFFX. There are auto loans in there along with the mortgages. Check out the Morningstar Portfolio page.

So RBFFX ain't for me. Could that change? Yep. That's why I run the charts weekly for all the Funds and read many more articles than the links I post.

See ya at the hall.

;)

;)

;)

;)

;)

( 2.9 / 1489 )

( 2.9 / 1489 )

Calendar

Calendar