| |

The Unemployment Number Wasn't That Bad If You Knew Enough To Expect It And If You Could Play On The Dark Side Of The Street. Otherwise, If You Were Long Stocks In Your 401a, It Was A Big Asphalt Face Plant.

Friday, July 3, 2009, 01:36 AM

It is not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change.

-- Charles Darwin

http://www.bloomberg.com/apps/news?pid= ... llNt3iGquQ

http://www.bloomberg.com/apps/news?pid= ... obeTB25ZeY

http://www.bloomberg.com/apps/news?pid= ... quXjXBNKo0

http://www.ritholtz.com/blog/2009/07/usa-spendinggov/

http://www.ritholtz.com/blog/2009/07/usa-spendinggov/

http://www.ritholtz.com/blog/2009/07/usa-spendinggov/

http://money.cnn.com/2009/07/01/markets ... 2009070116

http://rothkopf.foreignpolicy.com/posts ... washington

http://www.ritholtz.com/blog/2009/07/un ... more-30927

http://www.bloomberg.com/apps/news?pid= ... WJtkeFK5yU

http://www.bloomberg.com/apps/news?pid= ... cWAOCmAfVo

http://www.nakedcapitalism.com/2009/07/ ... 5-ltv.html

http://www.calculatedriskblog.com/2009/ ... st-95.html

http://www.ritholtz.com/blog/2009/07/up ... ear-chart/

http://www.bloomberg.com/apps/news?pid= ... v4JRht6M4Y

http://www.ritholtz.com/blog/2009/07/th ... or-supply/

http://www.bloomberg.com/apps/news?pid= ... pK3J1JYpXU

http://trueslant.com/matttaibbi/2009/06 ... -a-chance/

http://www.ritholtz.com/blog/2009/07/mi ... the-world/

http://www.bloomberg.com/apps/news?pid= ... RLpgz65Qto

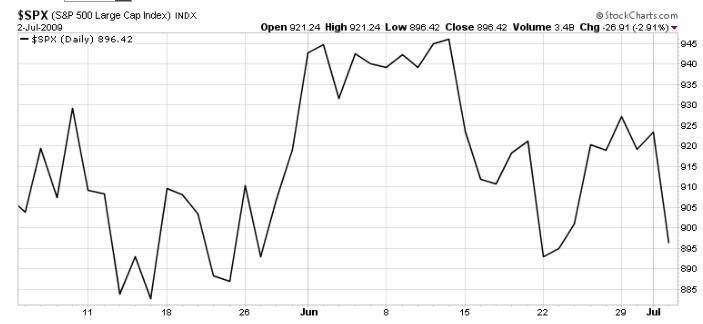

I got my answer. Unemployment re accelerating, work week hours at a record low, U6 unemployment @ 16.5% We've been going sideways and we ain't gonna launch upward in the immediate future. Employment is a lagging indicator, but we've been going up on "green shoots" and the deceleration of unemployment and housing depreciation. There have not been enough green in the shoots to tip consumer's mindset into the positive, unemployment re accelerated and every indication is that the housing workout will take much more time than hoped.

CLICK HERE

http://www.ritholtz.com/blog/2009/07/nf ... issection/

Here's my riff:

Decoupling;

Didn't work. The US sneezes, the rest of the world catches cold. Still true. Especially if they're awash in our mortgage backed securities and mortgages of their own. The reflation trade was just a trade, a headfake. Real economic recovery is still dependent on the consumer and the consumers mainstay is his job.

China will drive the world out of recession;

China is export driven and protectionist. Who are they gonna export to and who are they gonna buy from? Think about it.

Mortgage workouts;

Gimme a break. Fannie and Freddie can refi 125% LTV. So find me some borrowers who, 1) Need to refi and can/want to qualify for a $400K loan onna house now worth $325K. 2) Are then gonna take a non recourse mortgage and are going to turn it into a refi with recourse and that will require possible years to get them back to even. EVERYBODY WHO COULD FAKE AN APPLICATION, DID! Who's the new home buyers who will qualify under the new reality and bail everyone out at the old prices? This with the U6 measure of unemployment @ 16.5% (includes "discouraged, marginally attached,would like, and part time).

The banks are fixed and getting better;

Great profits with huge amounts of taxpayer supplied almost free money. Where do they put it to work? Does it make more sense to hang on to it and lose less of it while the economy finds the bottom, THEN loan it out?

I dropped into a local High End HiFi shop and mentioned that the week's unemployment figure came in at 467,000 vs the hoped for 325,000. The guy behind the counter went pale. This at a location that, if not recession proof, has the clients the least likely to hit the wall.

Things will eventually get better. But the time to be out of stocks was the 15 months previous to last March. The time to be back into stocks was March to the end of the day, June 30th.

Now we gotta reset reality as driven by 1)last quarters earnings, and 2) next quarters guidance.

Oh yeah, and financial markets news driven by rising unemployment, Iran and North Korea, and auto and manufacturing bankruptcies, municipal bankruptcies, Boeing DreamLiner delays, state bankruptcies and Afghanistan, and, and, and, and to a lesser degree by garden variety investment realities.

This insanely aggressive daytrader and momentum and position investor still has his 401a in the GIC and non governmental bonds. It's more important to keep what I made when times were good than to chase what may be there in a equivocal and possibly dangerous time..... There will be better days somewhere ahead.

AND CLICK HERE: http://www.youtube.com/watch?v=rUtlsk0l ... re=related

SATURDAY EVE

http://www.ritholtz.com/blog/2009/07/as ... ut-theory/

WTF????? Ban Short Selling??????

http://www.ritholtz.com/blog/2009/07/ba ... t-selling/

http://watchingthewatchers.org/indepth/ ... r-restrain

Stay Tooned...

( 3 / 1528 ) ( 3 / 1528 )

Consider This And The Last Two Posts To Be Of a Cloth... Notice How Old Guys Use Archaic Expressions? The Expressions And The Old Guys Didn't Start Out Archaic.....

Saturday, June 13, 2009, 04:09 PM

A man must not swallow more beliefs than he can digest.

-- Havelock Ellis

Wed

http://www.cnn.com/2009/WORLD/meast/06/ ... index.html

http://www.msnbc.msn.com/id/31403377/ns ... al_estate/

http://www.newsweek.com/id/202323

From the 6/13/09 Economist;

All told the outlook is bleak. In a few countries, the financial crisis has badly damaged the public finances. Elsewhere it has accelerated a chronic age-related deterioration. Everywhere the short-term fiscal pain is much smaller than the long-term mess that lies ahead. Unless belts are tightened by several notches, real interest rates are sure to rise, as will the risk premiums on many governments debt. Economic growth will suffer and sovereign-debt crises will become more likely.

Somehow, governments have to avoid such a catastrophe without killing the recovery by tightening policy too soon. Japan made that mistake when concerns about its growing public debt led its government to increase the consumption tax in 1997, which helped to send the economy back into recession. Yet doing nothing could have much the same effect, because investors fears about fiscal sustainability will push up bond yields, which also could stifle the recovery.

The best way out is to tackle the costs of ageing head-on by, for instance, raising retirement ages further. That would brighten the medium-term fiscal outlook without damaging demand now. Broadly, spending cuts should be preferred to tax increases. And rather than raise tax rates, governments would do better to improve their tax codes, broadening the base and eliminating distortive loopholes (such as preferential treatment of housing). Other priorities will vary from one country to the next. But after todays borrowing binge, doing nothing is no longer an option.

So it's like this.....ya gotta have a thesis.

Mine is that

the low of March this year was a panic low. The problems of 2007 supposedly had been fixed for good by early 2008 and by the time the Fall of 08 came around and things were headed for hell in a free fall pretty much everywhere, some serious downside momentum was in place. Coupla lower lows washed out all the sellers and left only shorts to sell.

Came the second week of March and people began to realize that even at 10 percent unemployment, 90 percent of the people would still be working, the employed and the unemployed would still be buying stuff, the government was shoveling money out of Ben's helicopters, and at some point inventories would be too low and products would have to be made and sold. Plus profit expectations had been driven into the ground by blind panic. So brave souls bought a little stock and the stretched to the downside rubber band snapped into motion. I caught a little of the move but missed that reality was ahead of expectations and I sold before the 1st quarter reports came out. DAMN!!! The reports were Better Than Expected. Stocks continued up without me and I fought myself over being late to the party vs arriving just as it cratered.

What now?

Well... stocks go too low and then go too high. There is a ton of money on the sidelines that missed the rally so far and CAN NOT MISS ANY MORE. There exist buyers desperate to buy. And interest rates are still fairly low. And the administration is cheer leading and papering over any signs of distress. And some places are still doing business and the rates of decline are slowing, possibly signaling a bottom and the headlines are about the bottom and the turn. But is it THE bottom...? Or just the end of a panic downdraft and the start of a long recession and extended trip across a flat economic landscape?

The rally looks tired. Stock prices pretty much discount a sizeable recovery. But the FED printed money like mad and now it has to borrow to fund what it printed. Bond buyers are offering less, fearing inflation, and that drives interest rates up and makes bonds a harder sell. That means that higher rates are needed on the bonds to raise the desired amount of money. That'll slow down refi's and new mortgages. The Fed will have to print more money and buy bonds to drive prices up and rates down, increasing fears of inflation. Which is the cause and not the cure. The Fed and administration have announced a flurry of plans, most of which are going nowhere. We have a ton of real housing inventory and an unknown amount of shadow inventory. The Fed offers the banks free money to start earning their way out of trouble. But the money is getting more expensive for the Fed to borrow and show me where the new business is for the banks to fund. Housing? Malls? Factories? Energy? Maybe... Wanna loan yourself some money through the government for a voucher to buy a new Chrysler SUV after you loan GMAC some money to fund your loan for the SUV? How about a house? Who's gonna buy your trade in? The Fed has entered into repo agreements with banks, taking toxic assets from them and giving back treasuries/cash. The mechanism by which the Fed can unload or make better the crap on its balance sheet and give it back to the banks/other investors is not apparent to me. The Great Unwind is still gotta happen and we're closer to the beginning than the end of flushing the crap away...

Check it out;

There is an important story in today's Telegraph about the increasing likelihood that some economically devastated U.S. cities may have to be partially bulldozed in order to survive. With cities like Flint, Michigan, having lost much of their rationale for existence, this should not come as a complete surprise. Nevertheless, this will be a difficult pill for "things will come back" America to swallow.

The government looking at expanding a pioneering scheme in Flint, one of the poorest US cities, which involves razing entire districts and returning the land to nature.

Local politicians believe the city must contract by as much as 40 per cent, concentrating the dwindling population and local services into a more viable area.

BLOW YER MIND...

http://www.telegraph.co.uk/finance/fina ... rvive.html

So my thesis is that we're going nowhere while things play out. I don't see a clearer road substantially up or down and I see a lot of resistance higher and a lot somewhat lower. But markets don't stand still. Fear and Greed and Hope and Despair will cause the markets to slosh around within a range. For how long? A week? A month? A year?

Check it out...

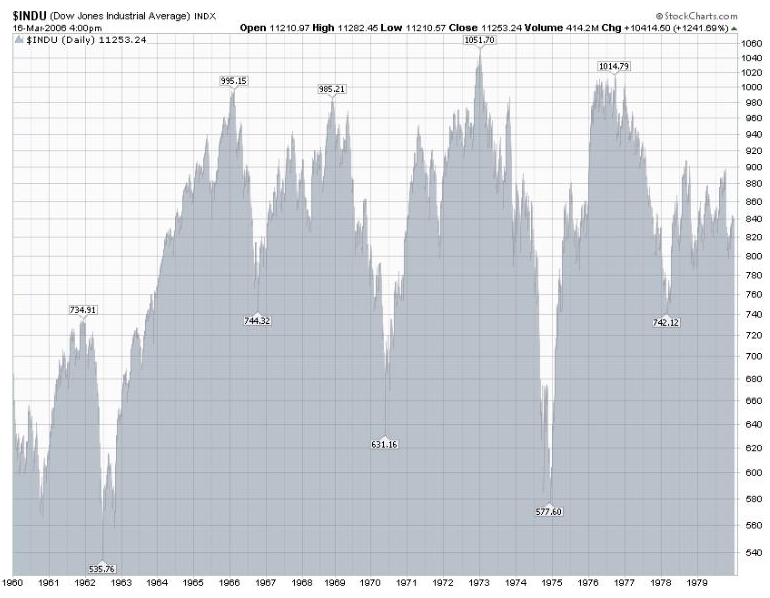

The Dow 30 was at 740 four times in 16 years and a ways above and below it. Buy and Hold? GIMME A BREAK!!!!! Tryin' to work with what the market gives me? Buy the dips and sell the rips? Make money that way? Prolly.... I'm gonna try

I committed a significant amount of my account to stocks earlier in the month to get back inna game. It didn't look that good, but I needed to re-engage my interest. So I made a dollar or two last week. Lately, not so much. I moved some money outa stocks and into the GIC this Friday, leaving some in stocks. There are buyers still trying to get into the party when the door opens for someone to leave... There may be a little more to go. But the easy money and a lot of it has already been made. The resistance seems greater to the upside than the downside and I'm more likely lighten up on stocks than buy more.

Tuesday Night

I lightened up some on stocks on Monday and I'm lightening up almost all the way tomorrow at the end of the day.

It's a mind game thing. Know what I mean, Vern?

Being all out of the market worked so well for sooo long that I got way too comfortable. I let waay too much money get away when the market spiked huge for three months and I watched it run away from me. Time to blow out the cobwebs, re-engage my brain, and get to work. I tossed a few dollars into the maw of the beast by committing about half my portfolio to stocks. I knew it was prolly way too late, But I hadda start somehow and somewhere. I watched enough bucks go up in flames to get my attention. Enough of that crap. Lemme see if I can make a dollar in a volatile and directionless market. If that's what we get....

Game on.

Stay Tooned

This Week's Post Is What Shoulda Appeared In Last Week's Post. That's Why The Quote At The Top Is The Same. I Couldn't Find A Better One For The Purpose.

Saturday, June 6, 2009, 02:05 PM

The one great certainty about the market is that things will always change. When we lose sight of that fact and dig in our heels on a particular viewpoint or thesis, it can create tremendous stress as we deal with an environment that may not appreciate our great insight.

Reverend Shark

Chartz and Table Zup @ www.joefacer.com

Lemme dig my way from outa a big pile of offput chores/obligations/ behests an' other crap an' I'll tell ya why I've averaged 11% return plus or minus since 9/04 an' why I'm up 55% plus or minus since 9/04 an' why IT PISSES ME OFF!!!!!

From MSNBC, Bloomberg, and Big Picture links below

I suspect that we will continue to need a trillion dollars' worth of deficit financing, fiscal stimulation, for several years at least," said Bill Gross, managing director of Pimco, which runs the world's largest bond fund. "This economy is still de-levering. It is still at the whim, so to speak, of savings vs. consumption. It is deglobalizing. It is reregulating. These are forces that slow growth."

I don't see where the second half recovery is coming from, said David Rosenberg, chief economist at Gluskin Sheff, a Torontobased investment firm. Until employment stops falling, this recession is still intact."

The government probably wants to win time for the banks, keeping them alive as they struggle to earn their way out of the mess, says economist Joseph Stiglitz of Columbia University in New York. The danger is that weak banks will remain reluctant to lend, hobbling President Barack Obamas efforts to pull the economy out of recession.

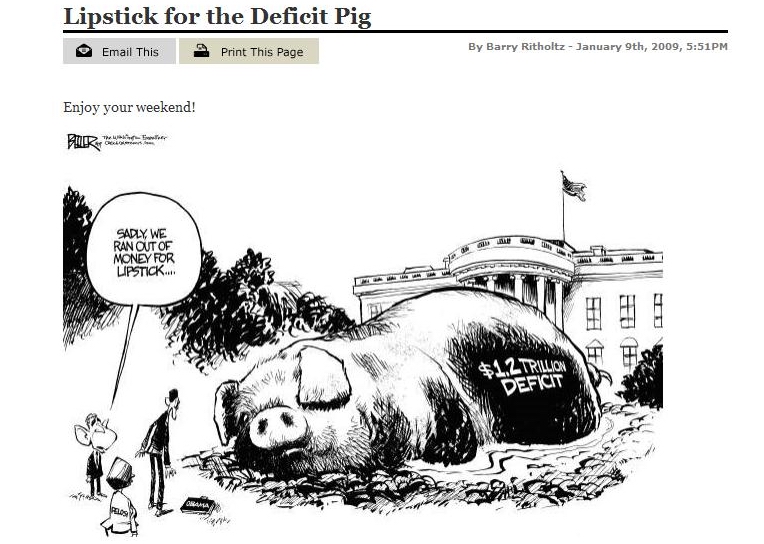

Citigroups $1.6 billion in first-quarter profit would vanish if accounting were more stringent, says Martin Weiss of Weiss Research Inc. in Jupiter, Florida. The big banks profits were totally bogus, says Weiss, whose 38-year-old firm rates financial companies. The new accounting rules, the stress tests: Theyre all part of a major effort to put lipstick on a pig.

Further deterioration of loans will eventually force banks to recognize losses that their bookkeeping lets them ignore for now, says David Sherman, an accounting professor at Northeastern University in Boston. Janet Tavakoli, president of Tavakoli Structured Finance Inc. in Chicago, says the government stress scenarios underestimate how bad the economy may get.

Citigroup also increased its loan loss reserves more slowly in the first quarter, adding $10 billion compared with $12 billion in the fourth quarter, even as more loans were going bad. Provisions for loan losses cut profits, so adding more to this reserve could have wiped out the quarterly earnings.

Wells Fargo

Without those accounting benefits, Citigroup would probably have posted a net loss of $2.5 billion in the quarter, Weiss estimates. In the five previous quarters, Citigroup lost more than $37 billion.

Wells Fargo also took advantage of the change in the mark- to-market rules. The new standards let Wells Fargo boost its capital $2.8 billion by reassessing the value of some $40 billion of bonds, the bank said in May. And the bank augmented net income by $334 million because of the effect of the rule on the value of debts held to maturity.

Wells Fargo spokeswoman Julia Tunis Bernard declined to comment, as did Citigroups Jon Diat.

The higher valuations Wells Fargo put on its securities probably wont last, as defaults increase on home mortgages, credit cards and other consumer and corporate lending, Northeasterns Sherman says.

Feds Optimism

These changes will help the banks hide their losses or push them off to the future, says Sherman, a former Securities and Exchange Commission researcher.

The Federal Reserve, which designed the stress tests, used a 21 percent to 28 percent loss rate for subprime mortgages as a worst-case assumption. Already, almost 40 percent of such loans are 30 days or more overdue, according to Tavakoli, who is the author of three primers on structured debt. Defaults might reach 55 percent, she predicts.

At the same time, the assumptions on how much banks can earn to offset their losses are inflated, partly because of the same accounting gimmicks employed in first-quarter profit reports, Weiss says.

Theres a chance that it might work, Columbias Stiglitz says of the governments attempt to boost confidence. If it does, then theyll look like the brilliant general. But all these efforts also bank on the economy recovering and housing prices not falling too much further. Those are not safe assumptions.

The package the White House hammered together to convert big, old, dying Chrysler into a smaller, healthier car company looks a lot like a massive violation of bankruptcy law. A few dissident creditors, namely three Indiana pension funds that banded together, remain defiant enough to say so.

The Chrysler plan seeks to extinguish the property rights of secured lenders, trampling the most fundamental of creditor rights in disregard of over 100 years of bankruptcy jurisprudence, the funds argued in bankruptcy court papers.

http://www.msnbc.msn.com/id/31121449/

http://www.newsweek.com/id/200991

http://www.msnbc.msn.com/id/31127909/

http://www.msnbc.msn.com/id/31143910/

http://www.msnbc.msn.com/id/31150694/

http://www.msnbc.msn.com/id/31110346/

http://www.bloomberg.com/apps/news?pid= ... _5hvV_xqHM

http://www.bloomberg.com/apps/news?pid= ... C3LxSjomZ8

http://www.bloomberg.com/apps/news?pid= ... iTT6yxgHSE

http://www.bloomberg.com/apps/news?pid= ... eYe_j75qvM

http://www.bloomberg.com/apps/news?pid= ... 2TV3oJtap4

http://www.bloomberg.com/apps/news?pid= ... tKbzvooAy0

http://www.ritholtz.com/blog/2009/06/it ... one-trade/

http://www.ritholtz.com/blog/2009/06/ho ... d-minuses/

http://www.ritholtz.com/blog/2009/06/pa ... rate-fell/

http://www.ritholtz.com/blog/2009/06/an ... ent-truth/

http://www.ritholtz.com/blog/2009/06/a- ... les-ahead/

http://www.ritholtz.com/blog/2009/06/th ... more-28300

http://www.ritholtz.com/blog/2009/06/tr ... licyuh-oh/

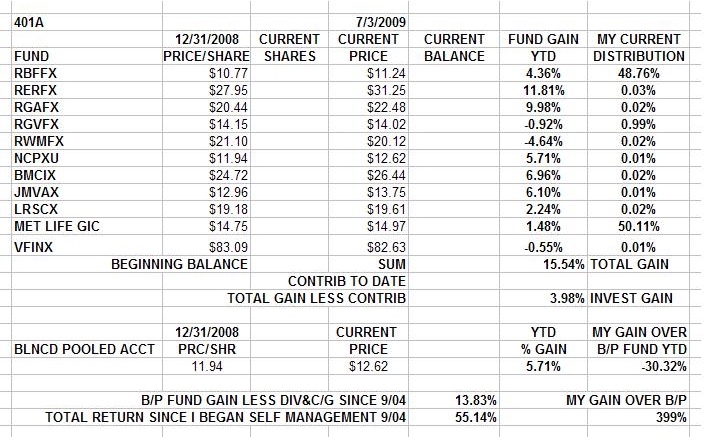

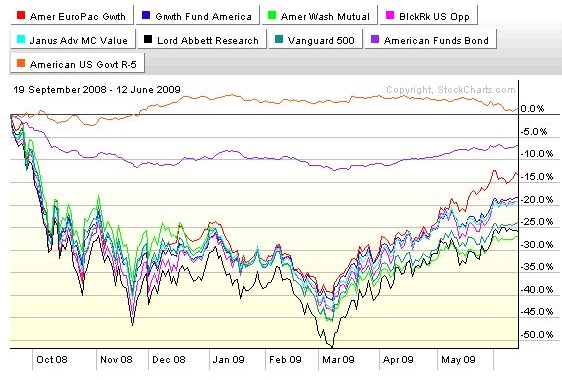

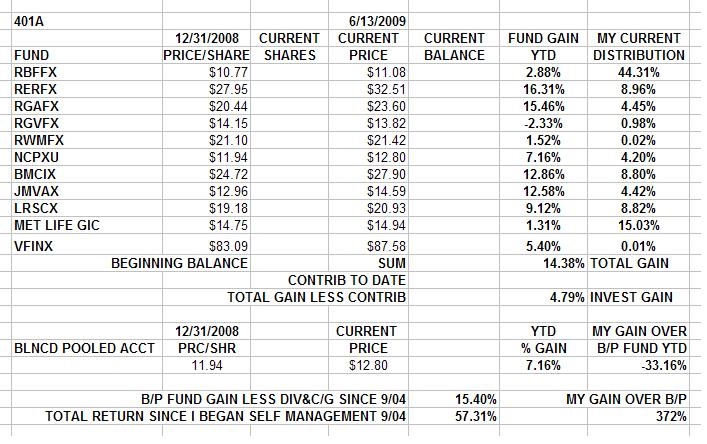

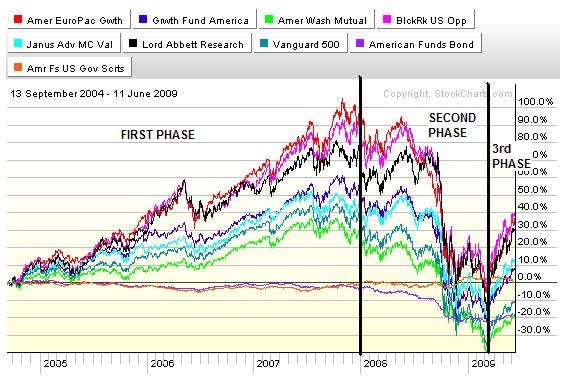

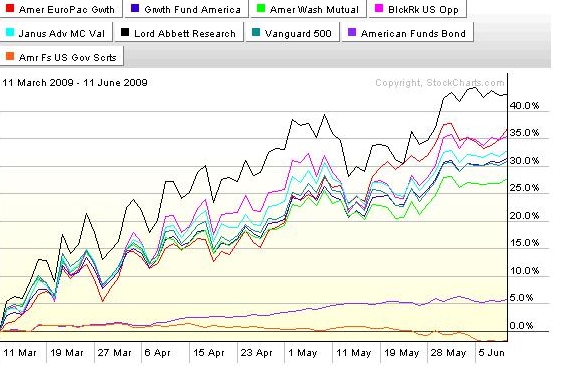

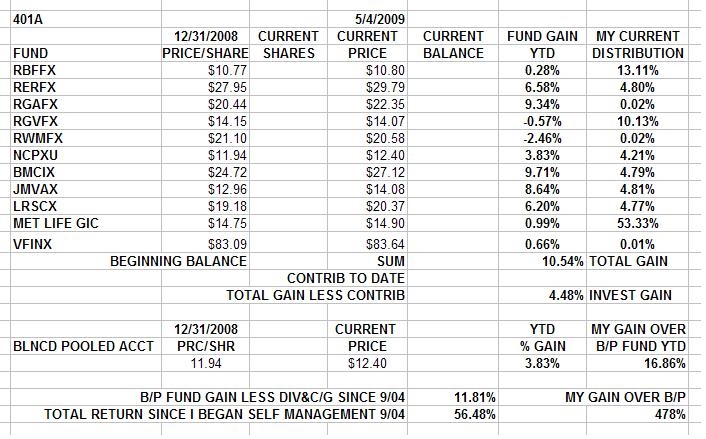

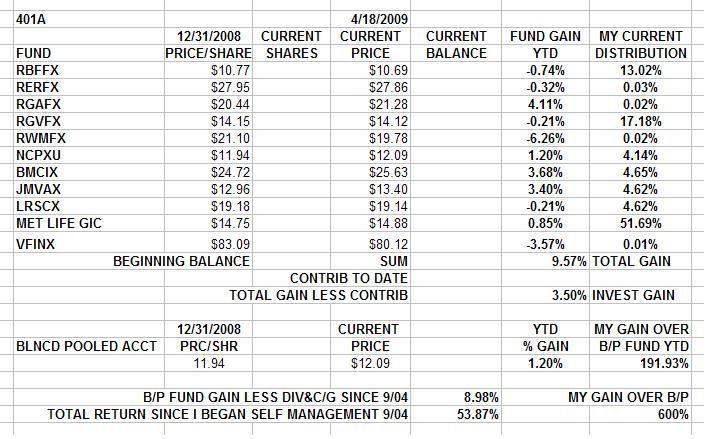

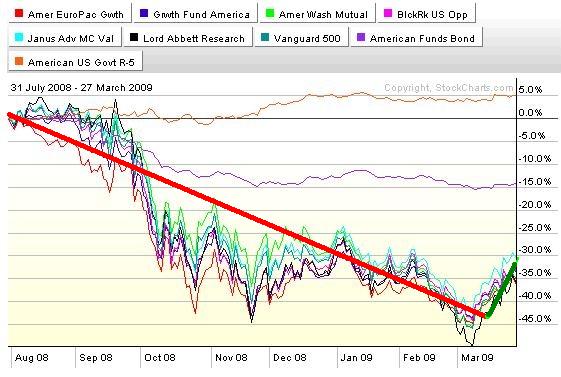

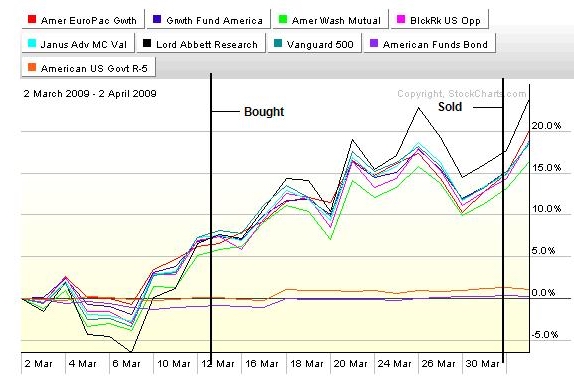

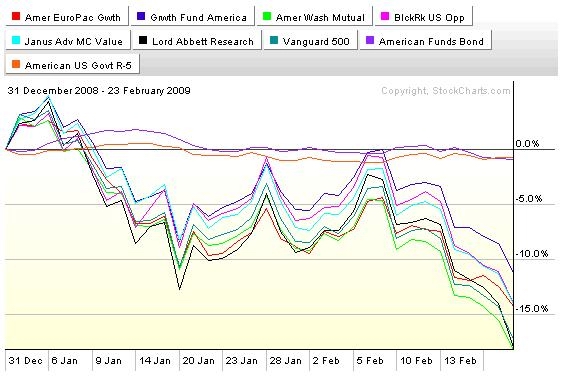

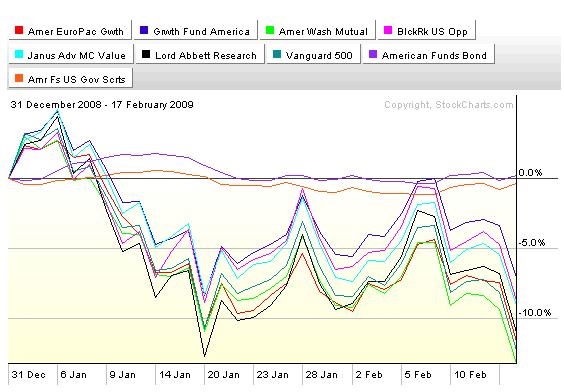

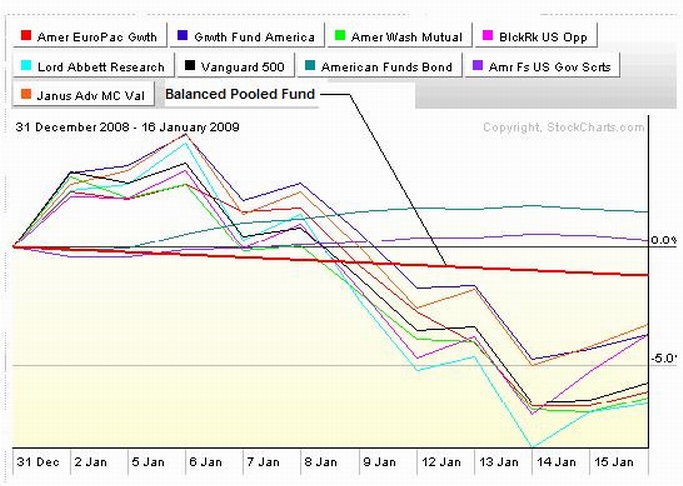

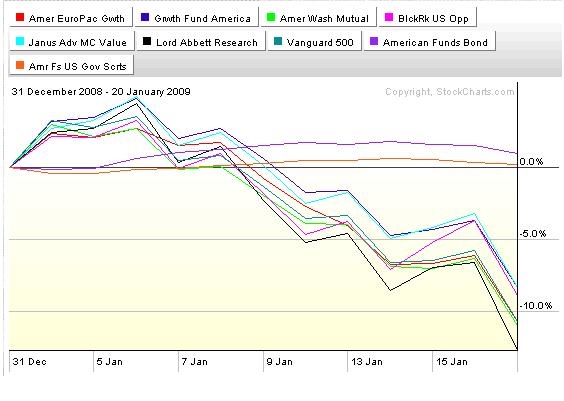

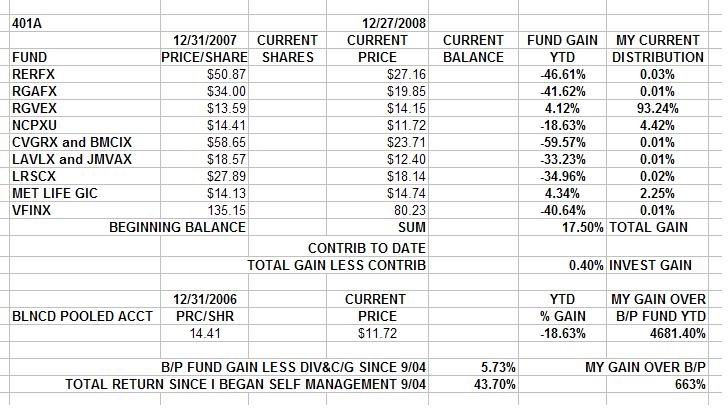

This is what the Funds available to the 401a have done since the time they became available (Since I got serious about 401a investing).

This is the period in which I went long and strong in stocks, at times almost 90% to 95% stocks.

This is the time period during which I was in cash (GIC) or bonds. Pretty kool so far.

This is the three month time period during which I was partially invested in stocks for about 4 or 5 weeks. IT PISSES ME OFF. For a trend follower intent on finding a trend and riding it as long as I could, I left WAY too much on the table when stocks turned up and kept going up. Lesson learned. I just moved a significant amount of my 401a back into stocks. Not because I think that there is a lot left to this move or that the market owes me what I missed out on. Rather, I did really well in a bull market 'cuz ya can't tell the idiots from the geniuses when everything is goin' up. I also did really well in a bear market because when hunkering down and playing possum is a brilliant strategy, it's really easy too. But now I expect a very volatile and range bound market. And that is a very different animal. It might be a bloody and frustrating market for an extended period. It also might offer the opportunity to make some aerious bucks with effort, smarts and luck. So i tossed some serious money into the action. Nothing quite like skin in the game to dial the focus and intensity up.

Stay tooned

Spiro T. Agnew, Dan Quayle, and now, Joe Biden. VP's who said what they thought. Big mistake. Link below

Saturday, May 2, 2009, 12:28 PM

My friends, no matter how rough the road may be, we can and we will, never, never surrender to what is right.

Dan Quayle

CHARTZ AND TABLE ZUP @ WWW.JOEFACER.COM

MAJOR MAJOR things going on at two Bay Area pension plans. Stay tooned while I do some reading and thinking... AN' THEN SOME WRITIN'; 'AHL BE BACH....

Sunday Evening....

Stay tooned for further information on a coupla Bay Area defined benefit pension plans. It's amazing how the similar situations can be viewed differently and responded to differently by different administrations. Somebody has it very right and somebody has it very wrong. Or not. How can you be sure without the necessary information? More to come as things become clearer.

Monday

http://www.newyorker.com/reporting/2009 ... table=true

http://www.ritholtz.com/blog/2009/05/se ... d-go-away/

http://www.ritholtz.com/blog/2009/05/mo ... i-blew-it/

http://www.ritholtz.com/blog/2009/05/ar ... ally-over/

http://www.bloomberg.com/apps/news?pid= ... refer=home

There is a lot of risk being in stocks now. I read the links I post here and a whole lot more beside. The risks I see ahead are huge and I'm very wary of the downside risk. I'm expecting a plunge down later in the year as the magnitude of the damage to the economy is finally recognized.

But for now there is a lot of reward to be had by being in stocks; bear market rallies are sudden and vicious and non rational and we got one. I've got a job to do; earn pension money. So below is my latest balancing act between greed and fear. But I'm not losing sight of the fact that this rally has claws and teeth and won't forget where its DNA came from.

Coulda done better; coulda done a WHOLE lot WORSE.

Got the latest pension mailing from the hall. Gimme a little time to do some analysis, then read about it here....

The Eye Of The Storm... Waiting For Your Dad To Get Home Like Your Mom Said You'd Hafta... Free On Bail... Seems Not So Bad At The Moment, But It's Lookin' Bad For The Future. I Think There Is Still Some Serious Shit Gonna Happen Soon Regardless of The Present Calm. What I'm Doin' 'bout It.

Saturday, April 25, 2009, 03:11 PM

Change hurts. It makes people insecure, confused and angry. People want things to be the same as they've always been, because that makes life easier.

--Richard Marcinko

CHARTZ AN' TABLE ZUP @ WWW.JOEFACER.COM

The GM/Ford/Chrysler debacle reverberates through our society. At the end of 2008, Prez Bush signed the Workers, Retirees, Employers Recovery Act of 2008. It was not because Workers, Retirees, and Employers could get something really good for almost nothing. It was because the fecal material hit the rapidly rotating oscillating rotary air mover.

Single employer pension plans were in large part, the sole responsibility of the employer to manage. They had good years and bad years in terms of money going into the plan and gains on the plan's investments. During bad years for the businesses, they wanted to be able keep some of the money that would have otherwise gone into the plan to make the current year's operating results look better. So rules were put in place that allowed them to project better investment gains for the plan in the future and project more contributions to the plan in the future so as to justifying cutting the current year's contributions to the plan.

Voila!!!

The companies books looked better businesswise and you were required to have more faith in the future pensionwise 'cuz you blew off takin' care of business this year. 'Course if and when you push too hard, and the company goes down in flames, the pension plan is really left in a huge hole. Like now. A lot of companies besides the car makers wanted short term relief last year. Last year's once in a lifetime crash (apparently "lifetime" means about 5 years) blew holes in everything financial and business and since the subprime thing was going to be contained to just one company or so, since the price of real estate only goes up, since the rest of the world would keep buying American stuff regardless of what happened here, since we were all safely diversified by being in stocks and bonds, tech and commodities, among different investment plans, since the government would keep everything afloat with the printing press, (pick your favorite discredited mantra) once things picked up by Summer of 09, everything would be kool. Pension funding would look good again and it would be back to business as usual.

It's not. Check out the links I've posted here in the past year.

Thursday I received a letter from a pension plan I'm a participant in. It went like this;

Federal Pension law divides pension plans into three categories;

Plans in the "Green Zone" are considered "Healthy". They are 80% or better funded and other conditions in the plan are supportive of the continued health and viability of the plan. All is cool and under control.

Plans in the "Yellow Zone" are "Endangered". They are less than 80% funded and there is nothing positive or supportive about the concept of "Endangered". By my understanding, Federal pension law prior to the Workers, Retirees, Employers Recovery Act of 2008 requires that the Trustees immediately improve the funding status of the plan. This can be done by adopting a higher level of funding (more money from the participants) or cutting the benefit accruals (less benefits allocated per dollar contributed).

Plans in the "Red Zone" are considered "Critical". They are funded at a level of 65% or less. Federal law requiring action in the case of "Critical" is not considered "Improvement", but "Rehabilitation".

If "Endangered" sounds bad, "Critical" sounds worse. Everybody like "Improvement". "Rehab" is pejorative. In both cases, there is a structure and benchmarks that must be met per a timetable to improve the pension plan's conditions until it is again sound.

The pension plan I'm a participant in was certified as "Green Zone" for the 2008 year. Their actuary has certified the plan a "Yellow Zone" plan for 2009.

The Workers, Retirees, Employers Recovery Act of 2008 allows the Trustees to "freeze" a plan's status at the 2008 level for the 2009 year, making this year's problem something that can be legally ignored. Like pinning the thermometer at 98.6. No fever, no problem. The pension fund can wait until 2010 to deal with the issue , if it doesn't go away on its own when you ignore it....

Unless the law is changed. To postpone doing what should be done immediately, which got GM to where it is now. Let's not go there until we get further down the page...

Anyway, the Trustees of the "Yellow Zone" pension plan intend to freeze the status and act on the shortfall in 2010.

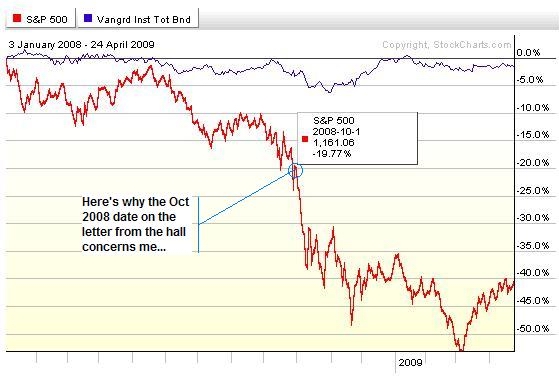

In a mailing dated October 2008, I was informed by another pension plan's Trustees, my main pension plan that I participate in, that the 94% funding of the 2007 year was no longer current. It further stated that the situation had deteriorated to the point that additional contributions to the plan would likely have to be made in 2009. I'm gonna guess that the language suggests that the plan went "Yellow Zone" in 2008, possibly earlier than the first plan mentioned. A lot has happened since October 2008 and not much of it has been good. I think I'm ready to hear more specifics from the Trustees on the matter.

A "freeze" in the status of the plan is like a "moratorium" on foreclosures. If things are going to get clearly better immediately, no problem. It's a good thing. If they are not going to get better, there's nothing like letting the problem build some momentum. Kinda like the gazillion dollars of taxpayer money that was shoveled into Wall Street to keep Brokers like Bear Stearns and Lehman Bros and banks like Citibank and Indy Mac and government agencies Ginnie Mae and Freddie Mac and insurance companies like AIG afloat. Uunh... they are still afloat...aren't they??!!? I mean it's not like we poured taxpayer money in and they went belly up anyway, except taking a lot of taxpayer money down with them... Is it???!!??!!?

I feel like I and anyone else like me interested in their pension need some current information from the Trustees.

Now.

Do we have a problem? If we do, how big is it and how do we fix it and when do we start?

It's not like we can rely on anyone else...

$20 Billion Short

...GMs pension system had a $20 billion shortfall as of Nov. 30, 2008, based on numbers the company provided the PBGC, said Jeffrey Speicher, a PBGC spokesman. (PBGC is the PENSION BENEFIT GUARANTEE CORP...jf) By law, the agency would be able to make up only $4 billion of that, he said.

The rest would be lost, Speicher said in an interview....

http://www.bloomberg.com/apps/news?pid= ... zS4bEfFmzs

http://www.1853chairman.com/2009/04/24/ ... ptcy-risk/

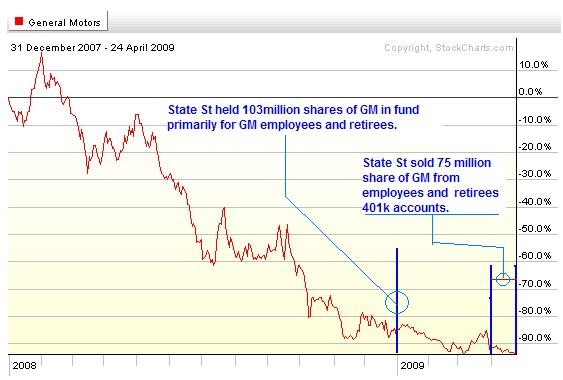

Of course, maybe the GM pension plan is in a lot better shape than it was in Nov 30 2008. Wanna bet that way? Just last week, the Trustee for GM's 401k announced that they had pretty much blown the GM stock from GM employees accounts...

April 25 (Bloomberg) -- State Street Bank and Trust Co., manager of a 401(k) investment fund for General Motors Corp. employees, has sold the majority of its shares in the automaker on concern that the stock could lose all value in a bankruptcy.

State Street sold 75 million shares, or about 12.4 percent of GM outstanding common stock, between March 31 and yesterday, Julie Gibson, a GM spokeswoman, said yesterday in an interview. It held most of those shares in a 401(k) fund for 29,800 employees and retirees. The fund is one of several options available in the GM employee-retirement savings plan.

http://www.bloomberg.com/apps/news?pid= ... 9lbsWMauyw

DAMN!!! It's like we didn't go through this already with employees of ENRON buried under ENRON stock in their 401k's....

More "Buy and hold for the long run and look at the account no more than once a year"?

Prepare for some heart wrenching tales of misery. Again, rethink the ENRON retiree and 401a story.

Pay attention to your pension and 401k. Vigilance is the price of security.

Stay Tooned....

Well....That Didn't Turn Out As Nearly As Well As I Hoped It Would......

Saturday, April 18, 2009, 02:17 PM

"No one that ever lived has ever had enough power, prestige, or knowledge to overcome the basic condition of all life -- you win some and you lose some."

-- Ken Keyes, Jr.

Chartz and Table Zup @ www.joefacer.com

Here's the dilemma; Big Time Caution was big time right onna way down. At some point, that caution would have/ will need to be tempered with aggressiveness, and at some point, my typically overconfident insanely aggressive nature will would have/ will need to be unleashed. In a perfect world, I'd a' gone WFO to the long side on 3/9 to date. Lookie here...

Instead, I was a week late to the party, only partially there and I left at least a coupla weeks early. I got some, but not nearly as much as I'd have liked. On the one hand, that's a little whiney coming from a guy with over 50% returns in his 401a over the last five years. On the other hand, I'm in position to take advantage of some serious compounding of returns and I don't like to watch potential returns fade away into the distance after doing this much work.

So.... 20% to 40% gains is many years worth of very good returns. That happened in 6 weeks. Is the party over? Am I coming out of the kitchen just as the cops come in the front and the flash mob comes in through the back door?

There is a huge amount of institutional managed cash out there that exhibited a lot more caution than I did and managers could be hearing from clients asking "WTF am I paying you fees for when the market is up 50% and I'm not innit??" There's money available on the sidelines to chase the market higher. Will it? Will it chase before or after a correction? Or two? How long will the disconnect between the market and the economy last and how will it resolve? Is this the mother of all bull traps? How much risk is left in a market that's down 50%? Why is everybody getting jiggy over fewer than expected foreclosures when the administration has been beating "voluntary" moratoriums out of the mortgage holders. Why is the administration getting stiff armed on the PPIP? (Hint...'cuz the banks see an "end around" that works better)

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://online.wsj.com/article/SB124016633014432579.html

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.msnbc.msn.com/id/30293461/

http://www.ritholtz.com/blog/2009/04/fo ... ts-ending/

http://www.pbs.org/wgbh/pages/frontline/meltdown/

http://www.ritholtz.com/blog/2009/04/su ... ales-fall/

http://www.ritholtz.com/blog/2009/04/fo ... urnaround/

http://www.ritholtz.com/blog/2009/04/fingering-aig/

http://www.ritholtz.com/blog/2009/04/bo ... t-selling/

http://www.ritholtz.com/blog/2009/04/ar ... reopening/

http://www.ritholtz.com/blog/2009/04/st ... e-summers/

http://www.ritholtz.com/blog/2009/04/gr ... r-suckers/

http://www.ritholtz.com/blog/2009/04/fo ... igh-in-q1/

http://www.ritholtz.com/blog/2009/04/se ... oversight/

http://www.ritholtz.com/blog/2009/04/be ... t-rally-4/

http://www.ritholtz.com/blog/2009/04/sa ... o-frannie/

http://www.ritholtz.com/blog/2009/04/fm ... ve-public/

http://www.ritholtz.com/blog/2009/04/ho ... chs-style/

http://www.ritholtz.com/blog/2009/04/ho ... the-world/

http://www.ritholtz.com/blog/2009/04/wo ... t-decline/

I changed my 401a allocation Friday. What was I thinking?

I was thinking of getting some exposure to the action, late or not, whatever direction it may be. It is DANGEROUS to chase stocks big time after a 25% or 50% move. That is not how the game is played. The last one in is invariably an innocent or a fool. Who'd we sell Rockefeller Center and Pebble Beach to at the top in the late 80's? The Japanese. We quoted the price in yen and it was cheap by Tokyo standards. Who bought PALM at $800 and Enron at $100 in 2000 and rode them down to a dollar or two in 2001? People who planned on selling when it doubled and then waited to get back to even... )Of course, we're not AT a top. And I'm neither an innocent or a fool. And stocks will at some time, go up.

That said.... If ya wanna find darkness and despair, ya can with lookin' too hard. Check out the last 6 weeks links. Eighteen percent unemployment in Elkhart ID. Don't look it as a high paid union worker legacy problem. Most of the RV and industrial shops that have gone down were non union. Jobs didn't go to where labor was cheaper... they ceased to exist. White collar GM employees (clerks and managers) facing losing pensions or reduced pensions. money out of the economy. Seniors scrabbling after Micky D's jobs in competition with the teeny boppers. Autos and real estate and financial and retail and muni and manufacturing jobs gone away. There has been a bounce the last month or so....but last year /first of this year the economy looked down into the abyss. Everyone slammed production and employment and orders down to less than maintenance levels. And like in the 80's, when we had 12% unemployment (apples and oranges, they've since jiggered the numbers) when you subtracted the unemployed from the employed, you still has people with jobs and income to buy with. So we've bounced. Sales and production have picked up and the loss of jobs have slowed. But the direction of the economy is still down. The economy can and will get worse, and there are still jobs and money to be lost and written down.

But the market discounts the present and buys the future. If investors think they see the bottom, or the slope lessening as we approach the bottom, they will look across the valley bottom to the upward slope of the other side. The market CAN go up as things get worse. Or not.

So I've taken a single step into the action. If there is still action to the upside, I'm there. If it shows legs, I can take a second step. If the market does a 100 MPH faceplant well below this years lows, I'm only a step away from the door, and 85% intact for the ride up off the real bottom whenever it happens.

Call it a calculated risk...and make no mistake, the emphasis is on risk.

Stay toooned.....

I think of myself as aggressive and focused and I've seen 145 MPH and still accelerating on my street bike running toward Turn One at Thunderhill, and I've run my race bike there even harder .... but DAMN, some of them old guys....hangin' on at 150 MPH through the measured mile after the bike has topped out on a very long run up!!!!!

http://en.wikipedia.org/wiki/Rollie_Free

First There Is A Mountain, Then There Is No Mountain, Then There Is. From Donovan to The Allman Bros. Who 'da Thunk?

Saturday, April 4, 2009, 11:31 AM

It is the markets job to reallocate money from the ignorant to the intelligent, from the lazy to the hard working and studious; from the naive to the educated, and from the speculator to the investor.

Barry Ritholtz

CHARTZ AND TABLE ZUP @ www.joefacer.com

The one great certainty about the market is that things will always change. When we lose sight of that fact and dig in our heels on a particular viewpoint or thesis, it can create tremendous stress as we deal with an environment that may not appreciate our great insight.

Reverend Shark

So maybe we had a bottom or the bottom or whatever and the markets bear market bounced into earnings. I reallocated 50% into stocks to take advantage of the better market conditions and earned some money for my retirement. Then I lightened my stock allocation into earnings season because the risk of holding into what was expected to be gawdawful earnings numbers was too high for my 401a account. I knew I was going to be out of stocks early to stay within the 401a rapid trading restrictions. So being out while the market goes up is part of the game. Sure enough, the market continues to go up. This is my 401a account and I don't like to chase the markets up. The rules of this game do not favor such. But, if I buy back in, would I be chasing the dregs to the drain and goin' down? Or would I be buying into a new long term bull market? Damn good question. It is something to worry about for the next coupla days. But I'll get an answer next week. A little uncertainty about booking profits ain't such a cross to bear. Nobody ever went broke bookin' profits... But a lot of people get their face torn off holding for the long run or waiting to get back to even. Twist the Wrist and ride on.

http://videos.streetfire.net/video/Wing ... 146752.htm

Chaos And Entropy Abound. Planned Events Go Awry and Random Events Effect Change Far Beyond Rational Expectation: Finally!!!! Something I Can Work With......

Saturday, March 28, 2009, 02:47 PM

One of the most difficult investing skills to master is being persistent and confident while not crossing the line to being stubborn and obstinate. It is a very fine line and you will never get it quite right now matter how hard you try.

Reverend Shark

Chartz and Table Zup @ www.joefacer.com

Stay Tooned....

Here's A Good Chart... A Variation Onna Double Top or Rounded Bottom....

Livin' Inna USA.... Somebody Get Me A CHEEZEBurger!!!!!

http://www.ritholtz.com/blog/2009/03/pp ... more-22802

http://www.ritholtz.com/blog/2009/03/kr ... itization/

http://www.ritholtz.com/blog/2009/03/wh ... ith-bonds/

http://www.rollingstone.com/politics/st ... g_takeover

http://www.ritholtz.com/blog/2009/03/ne ... uary-2009/

http://www.ritholtz.com/blog/2009/03/bu ... out-money/

http://www.ritholtz.com/blog/2009/03/in ... d-housing/

http://www.ritholtz.com/blog/2009/03/ho ... tion-work/

http://www.ritholtz.com/blog/2009/03/in ... d-housing/

http://www.ritholtz.com/blog/2009/03/gr ... s-amnesia/

http://www.bloomberg.com/apps/news?pid= ... refer=home

SUNDAY

More to come; But for now suffice it to say that investment risk is markedly less than in the recent past. Things have ALREADY gone to hell. We're half way to zero. We've seen a bottom and I reallocated 50% back to stocks. Check it out below in previous week's posts....

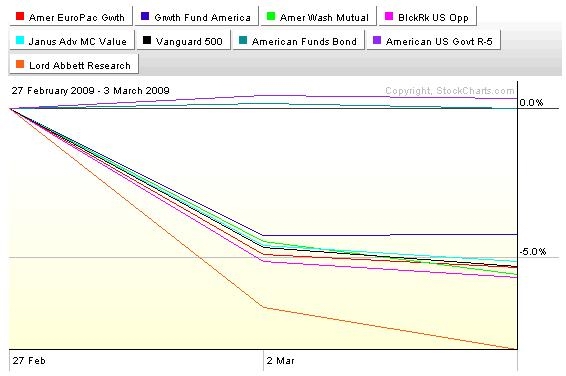

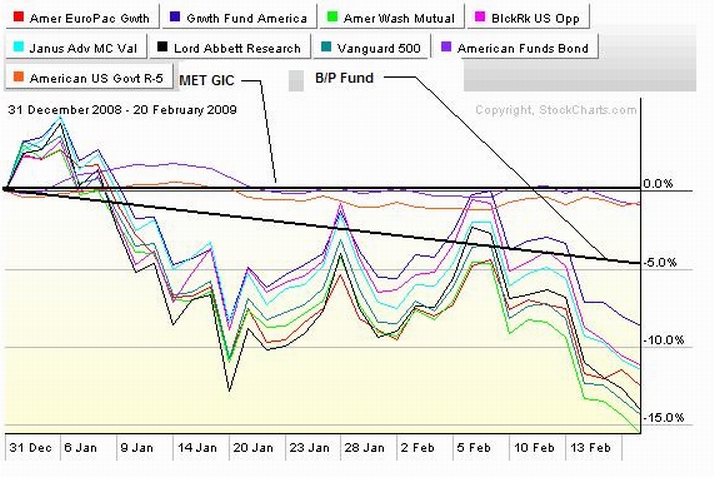

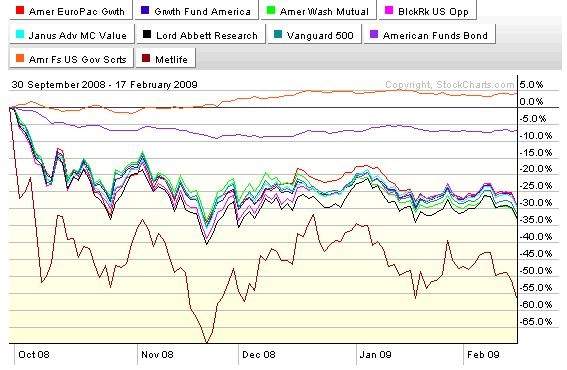

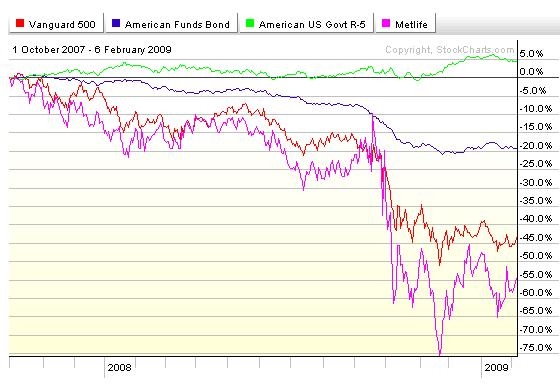

But then on Friday, I pretty much cut my exposure to stocks by 50% to 25% and put my money where I had been very wary of doing so, in MET Life. Here's what it looks like...

We've seen A bottom, but maybe not THE bottom. Earnings will be terrible. The economy is still going down... not as fast as it was, but down is still the direction. There is a bunch of mortgages being applied for.... but they are refi's. The stock of new houses and repos is still huge. The FED is pushing on a string. There are still jobs to be lost. Stimulus dollars to the state are being spent on subsidies to promote social issues and to paper over budget issues; job creation are still hanging fire. The Bad News on GM and Chrysler is gonna hit tomorrow (Monday) and it may not suit Wall St. (or me) This minute I'm more interested in keeping what I made than losing out on further gains. CHECK IT OUT.

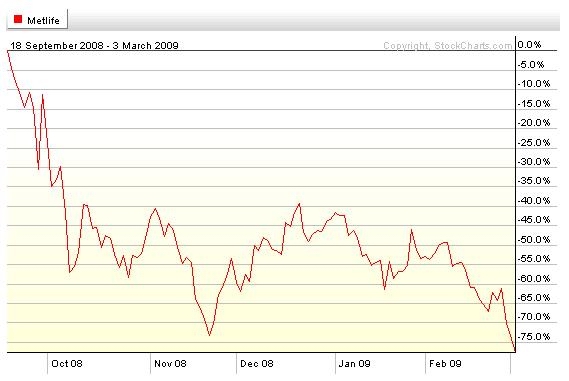

The red line is what I've missed by being in cash and the green line is what I've made by being in stocks. CLICKIT!!!! There will be a time and place when I'm looking for more exposure to stocks. Here and now ain't it. I'm still concerned about MET LiFE's safety. But by now I'm willing to bet that the tax payers will back them up.... Stay tooned.....

Oh, yeah....There's two couples that I've been talkin' to that need to pull the trigger on the refi's. You know who you are!!!!!

MONDAY

AMAZING!!!!

WEDNESDAY

Lookie Where We Came From....

I reallocated further toward a larger cash/smaller stock position today. The trend is still down, the economy is deteriorating more slowly but still deteriorating, the news is still equivocal, there are corporate and employment issues, and although we are getting closer to a bottom and a recovery..... there still is a substantial risk of revisiting recent lows. I've managed to avoid losing a huge percentage of the 401a. I'm gonna go with what has been working.

See how long and far we went down? I don't think we are going back up so fast that I won't be able to reallocate back to stocks in time to make a dollar.

THURSDAY

Look at the chart above. Smokin' upside move in a month. Now look at the same run up onna chart above that. Not so smokin'... What's wid dat? People are giddy over the move. "End of the Bear" an stuff... Or maybe not. Maybe things are still bad and getting worse and this was a bear market bounce. Too much of the move is non-rational in terms of the economy. More unemployment, more retrenching for the consumer, fewer bucks spent, more saved, less produced, less transparency with the relaxing of mark to market, the stimulus money not yet out to the public, and other stuff yet to come.

"Buy the dips and sell the rips"

Easier said than done. That was a BF dip we had goin' for the last year. Buyin' the "dip" too soon woulda ripped your face off and sellin' the "rip" after the long way down woulda left you still buried in a shallow grave.

Easier to buy the start of the rip and lock in some profits while you still have them or cut the losses quick if you were wrong about it beein' a rip.

Should I have held on? Dunno. We'll see. So many stocks up 10%-30% on no good economic news or objective improvement in business conditions. Not that it doesn't make me uneasy to be out of the market. Just not all THAT unesy.

So I'm out for now.

Stay tooned...

HOW DO I DO IT? "BRUTE FORCE AND DUMB CLUMSINESS." IT'S ON MY FAMILY CREST!!

Sunday, March 15, 2009, 05:00 PM

Our activity as investors is not to try to identify tops and bottoms - it is to constantly align our exposure to risk in proportion to the return that we can expect from that risk, given prevailing evidence.

-- John Hussman

CHARTZ AND TABLE ZUP ON WWW.JOEFACER.COM

Friday I moved a very significant portion of my 401a into the market. I have an overall plan and some criteria by which to decide alternate actions and reactions as circumstances and inclination require.

Coupla things about the table. I'm still 50% bonds/cash. This is NOT the bottom. I'm NOT all in on a secular bull move off the long term bottom. I've spread small amounts of money in every domestic stock fund available except one, VFINX. I'm not in VFINX because I don't like the rapid trading limitations for Vanguard funds. The reason I've used small amounts in a lot of funds is so that I can get back out in 2 days and stay within the rapid trading restrictions of all the funds. The reason I'm in every domestic fund including RWMFX, which I think is a real dawg, is that,

1) I want maximum exposure to the market without running afoul of the rapid trading restrictions and I'll take the added exposure in a dawggy fund, accepting lower returns for the ability to get out cleanly if it doesn't go the way I expect.

2) I believe the risks are too great in the foreign stock fund.

Here's a quick rundown of Three possibilities at play here;

1) We've got an oversold bounce. We've had a buncha days down in a row. Everyone who had the inclination and means to sell, did so. They got so far out there, that they got nervous and have stopped selling and covered their shorts or had nothing left to sell into short covering or the everyday buying that started the move up. If that is so, the move up is over/will be over within a day or two and I'll bail out and go back to cash for a small loss.

2) We've got a Bear market rally workin'. The bottom is STILL NOT IN. But we'll see a sustained upward move similar to the sustained downward move we just had, but taking us only part of the way back up. It'll be quick and vicious, and it'll end when we reach a technical resistance level, or we get a news item that affects investor psychology, or when fear and exhaustion overcomes greed. Rather than having the rug pulled out from under me immediately, as per #1 above, it'll happen later when I'm feeling good about finely making a dollar in stocks in the 401a. Between recognizing it's time to sell and actually getting out, I'll probably lose some money. That's how it works. and if it works out well I might make a coupla dollars and keep some of it too. Works fer me,Tweety bird.

3) I'm totally wrong and we start a new bull market and I never get my sell signal and I'm forced to go all in on stocks and make a lotta money being long stocks. That works for me too. But I don't see it.....

What I intend to try is not without risk. Then again, neither is buying, holding and not looking at my 401a but once a year. A day will come when the coast is clear to load up on stocks and stay that way. I just don't know when that'll be.....

Know What I Mean, Vern?

Stay Tooned....

http://www.ritholtz.com/blog/2009/03/fr ... 0-billion/

http://www.msnbc.msn.com/id/29708346/

http://www.ritholtz.com/blog/2009/03/ne ... -insurers/

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.ritholtz.com/blog/2009/03/st ... tle-banks/

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.ritholtz.com/blog/2009/03/ha ... ottom-yet/

http://www.nytimes.com/2009/03/14/busin ... .html?_r=1

http://www.bloomberg.com/apps/news?pid= ... refer=home

WEDNESDAY

NOT HALF SHABBY

I've been allocated away from stocks for a long time. This week's reallocation is a huge change for me. I'm fairly confident that there has been "A" turn in the markets, but not necessarily "THE" turn. So I'm self directing my 401a as was intended to increase my exposure to stocks when the risk /reward is more favorable. Fifteen months ago the SPX was at 1500, with the risk/reward being some measure of appreciation upward as the reward and 100% down being the risk. Last week the risk down was still 100%.... but from 50+% down compared to 15 months ago... If you don't believe that the market can go to zero, ya gotta think that the risk/reward here is fairly righteous in your favor, especially compared to 2007.

Now I've gotta keep concentrating on avoiding losses and add working on making gains to the mix.

HOWEVER...

I posted the above after lookin' at charts. After catching up on my readin', it is clear that the FED did something very very good or very very bad today. There is emotion, incredulity, and anger everywhere and EVERYONE has an opinion. I'm workin' on mine. Rhere is NO DOUBT that this will affect the market big time. It's the direction that is so hard to figure out....Stay Tooned...

Friday, March 13, 2009, 01:54 AM

I'M THINKING OF GOING LONG SOME STOCKS INTO THE WEEKEND. THIS IS CONCEIVED AS A RENTAL AND I'M DEFINITELY NOT GETTING MARRIED TO THE IDEA OF HOLDING STOCKS LONG TERM. BUT WE WENT STRAIGHT DOWN FOR A REALLY LONG TIME AND LOOKED LIKE WE WERE WAY OVERSOLD. AND SOME NUMBERS ON THE ECONOMY DON'T LOOK AS BAD (STILL GOING DOWN, BUT SLOWER) AND THE MOOD OF THE STREET SEEMS BETTER, WE'VE CONTINUED TO PERFORM ON THE UPSIDE AND THE ENTHUSIASM SEEMS TO BE CONTAGEOUS. SO WE MAY GET A TWO TO FOUR WEEK BEAR MARKET RALLY. IT'LL BE BRUTALLY SHARP AND SUDDEN AND TEMPORARY, IF IT HAPPENS, BUT A PIECE OF IT WOULD BE NICE TO CAPTURE.

OR WE MIGHT HAVE JUST A BOUNCE GOING, FIZZLING OUT WHEN EVERYONE DECIDES IT'S TOO RISKY TOO HOLD OVER THE WEEKEND, AND REALLY MELTING DOWN IF SOMETHING BAD HAPPENS OVER THE WEEKEND.

AND IF AGAINST ALL ODDS, THAT WAS THE BOTTOM, (FAT CHANCE) THERE WILL BE LOTS OF TIME TO GET IN AND A SLOW START WON'T MATTER.

EITHER WAY, I'M NOT INTENDING TO GET IN ANY DEEPER THAN I CAN CLEAR OUT IN A DAY OR THREE IF SOMETHING GOES SOUTH. I'LL DECIDE MID DAY....

AND YEAH I KNOW I'M SHOUTING, BUT THIS IS A BIG AND SUDDEN CHANGE AND I WANTED IT AND MY RESERVATIONS ABOUT THE CHANGE TO BE EMPHASISED.

[ view entry ] ( 1121 views ) [ 0 trackbacks ] permalink ( 2.9 / 388 )

Defined Benefit Pensions Plans In Trouble And Why Doin' The Smart Thing in my 401a Feels So Painful...

Saturday, February 28, 2009, 02:22 PM

Ninety percent of politics is deciding whom to blame.

-- Meg Greenfield

CHARTZ AND TABLE ZUP @ WWW.JOEFACER.COM

UPDATED CONSTANTLY....OR NOT. EDITS OF EXISTING POSTS NOT CALLED OUT.

LOOK FOR THE DAY OF THE WEEK FOR NEW ADDITIONS.

I talked this week with a friend who participates in the boilermakers' defined benefit pension plan . He said that he had received a letter recently from the pension fund announcing that all pensions were to be halved. This sounds like what would happen if the pension plan were to fall low enough in assets to trigger the Pension Benefit Guaranty Corp (PGBC) guaranty. As I understand it, when a pension plan's assets vs their liabilities fall enough, the PBGC steps in and cuts pension payouts by a complex formula that ballparks as roughly a 50% cut. All non monetary benefits are canceled and the PBGC loans the pension plan funds to meet its obligations until the plan can be funded adequately with more contributions. I have not seen the letter, but I consider him to be a reliable sources given that what I got was a conversational summary of the letter.

I also talked to a friend who attended a recent meeting at the electricians local who said he was told that if things did not change for the better, that the defined benefit pension plan would fall below critical funding requirements by 2014, requiring default. His pension plan had reduced the pension credit paid for last year and he was told that it would be cut this year by an additional 40%.

I received the usual yearly legally required letter from my defined benefit pension plan last year and it was noted that additional contributions would be required this year to maintain funding. This is not surprising, given the chaos in the financial markets, but it would be a damn good thing to have enough details to be understand what the situation is and to be able to plan and react appropriately.

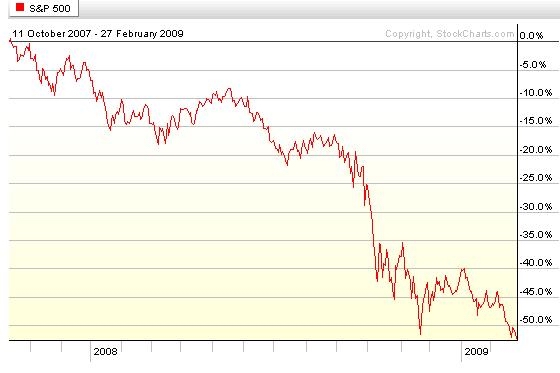

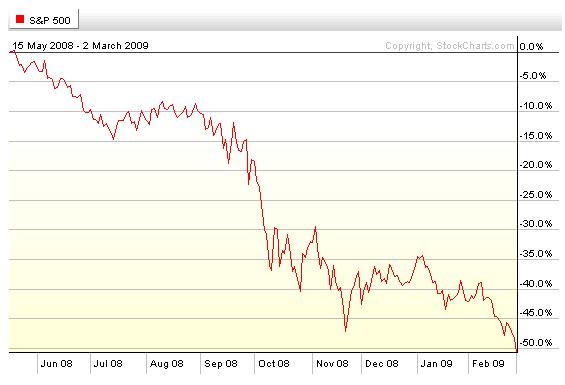

Last November was the point of maximum panic. The current hope for a recovery in the market has been the belief that November was THE LOW for this cycle. Now we are about to find out if this is true. We hit the low last week and we test the November low this week. The main difference this time is that it is not a "fire in the theater and only one exit" panic. It is more of a abandon all hope 'cuz not only is it REALLY REALLY bad, no matter how bad yesterday was, today's news just gets worse.

HANG ONNnnn!!!!!

http://www.ritholtz.com/blog/2009/02/gdp-is/

http://www.ritholtz.com/blog/2009/02/ne ... -down-482/

http://www.ritholtz.com/blog/2009/02/at ... e-zombies/

http://www.ritholtz.com/blog/wp-content ... 205938.gif

http://www.npr.org/templates/player/med ... =101144610

http://www.ritholtz.com/blog/2009/02/wo ... get-worse/

http://www.msnbc.msn.com/id/29453718/

http://www.ritholtz.com/blog/2009/02/un ... the-world/

http://www.ritholtz.com/blog/2009/03/q4 ... m-and-wfc/

http://www.2000wave.com/gateway.asp

http://www.newsweek.com/id/186957

http://www.msnbc.msn.com/id/29455792/

http://www.ritholtz.com/blog/2009/02/de ... recession/

http://www.ritholtz.com/blog/2009/02/golden-parachute/

http://www.nytimes.com/2009/03/01/magaz ... .html?_r=1

http://www.ritholtz.com/blog/2009/02/na ... ew-n-word/

http://www.dilbert.com/strips/comic/2009-02-25/

http://www.ritholtz.com/blog/2009/02/bl ... rey-goose/

http://www.ritholtz.com/blog/2009/03/me ... roit-7500/

http://www.theaustralian.news.com.au/bu ... 43,00.html

http://papers.nber.org/papers/w14753

http://www.ogj.com/display_article/3547 ... ion-costs/

http://www.nytimes.com/2009/02/28/opini ... wanted=all

http://business.theglobeandmail.com/ser ... iness/home

http://www.shanghaidaily.com/sp/article ... 392677.htm

http://online.wsj.com/article/SB1235776 ... od=testMod

http://www.economist.com/printedition/d ... D=13184655

http://www.time.com/time/magazine/artic ... 89,00.html

http://www.nytimes.com/2009/03/01/magaz ... wanted=all

http://isthisthebottom.com/

As per the charts on my website, www.joefacer.com, My funds are virtually all in bonds or equivalents. AGAIN, Nothing Ventured, Nothing At Risk...

The US and European credit markets are totally stretched and weighed down with toxic assets. There is no motivation to loan and a lot of companies that may yet fail.

It is a world wide crisis with great risk to the political and financial integrity of European Union.

China is as awash with factories and unemployment as we are with debt and is as awash with capacity as we are with securities. They are as short customers as we are of good loan prospects and a lot farther away from creating domestic consumption than we are.

The European economic situation may engender geopolitical strife as national security may be threatened in a number of countries.

It looks more and more like GM and Chrysler may get prepackaged bankruptcies or something similar.

The stress test riff of the Fed looks like yet another case of too little/missing the point.

There are more shoes to drop as the 6% plus drop in GDP for '08's last quarter may accelerate. Insurance companies may be the next shoe.

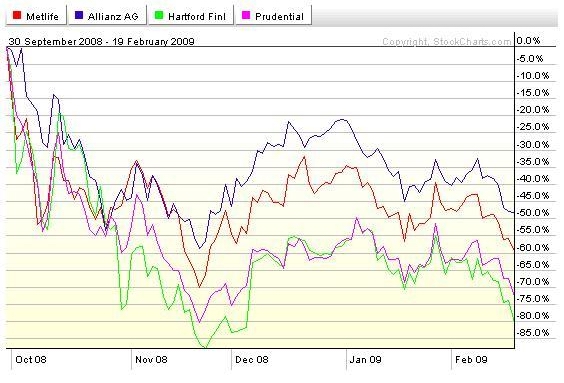

So the Met Life GIC pays the best of my 401a options, is stuffed full of well rated bonds and securities, and would be the place I'd most like to put my money. But the bonds are well rated the same ratings agencies that rated the mortgage bonds that almost cratered the global financial markets. You've seen the stock chart for MET here in this blog. I listen to what the market says. Its the smart thing to do.

SO... I'm big time in bonds with virtually no stocks in my 401a. I'm leaving way too much money on the table as the bond funds bleed a little here and there. It hurts. And ordinarily I'd just go the the GIC for relief. But I just can't expose my savings to one company, non diversified risk. It's just that this time doin' the smart thing is also a little painful....

MONDAY

Blew right through the prior low.

LOOK OUT BELOW!!!!!!!!!

TUESDAY

GAWD WHAT A CRUMMY TWO DAYS!!!!

'NUFF SAID

THURSDAY

WAS IT TOO LATE TO SELL MONDAY?

NOPE. BETWEEN FRIDAY AFTERNOON AND THURSDAY AFTERNOON, I'D A LOST A PRETTY GOOD YEAR'S WORTH OF RETURNS IF I HAD STILL BEEN IN THE MARKET....

GAWD WHAT A CRUMMY 4 DAYS!!!!

WOULD I BE WORRIED ABOUT HAVING MONEY IN MET LIFE? IF I HAD MONEY IN MET LIFE In THE FIRST PLACE? MORE THAN 'NUFF SAID...

Stay tooned...

Wednesday, February 25, 2009, 10:18 PM

"Sometimes I lie awake at night, and I ask, 'Where have I gone wrong?' Then a voice says to me, 'This is going to take more than one night.'"

-- Charles M. Schulz

CHARTZ AND TABLE ZUP @ WWW.JOEFACER.COM

UPDATED CONSTANTLY....OR NOT.

LOOK FOR THE DAY OF THE WEEK FOR NEW ADDITIONS.

Learning to sell is a great exercise. It sets you up with the mindset that investing has two polarities in a number of parameters. Prices go up and down, Investing time is made up of today and all the tomorrows. You can buy and sell to increase or decrease your investment in any position. Time and price happen happen pretty much on their own. Buying and selling are up to you. Pretty kool..... Especially since I sold long ago and the chart below, while ugly beyond belief, will only be relevant when I buy back in. JEEZUS!!! THE CHART BELOW COVERS 35 DAYS!!!! OUCH!!!!!

MONDAY

JEEZUS!!! THE CHART BELOW COVERS 36 DAYS!!!! OUCH!!!!!

http://www.ritholtz.com/blog/2009/02/while-rome-burns/

http://www.ritholtz.com/blog/2009/02/while-rome-burns/

http://www.investorsinsight.com/blogs/j ... stone.aspx

Further, most investors rely on research that always touts winners. Where stock researchers might say there is nothing worth buying or holding during a terrible market, the most popular and relied-upon fund research doesn't work that way, because it's more a description than a recommendation. Thus, 10 percent of all funds in an asset class will get Morningstar's top five-star rating, regardless of market conditions. Another 22.5 percent get a four-star rating. And 20 percent of every peer group earns Lipper's top marks for total return, consistent return and preservation of capital.

Chuck Jaffe

The whole article is here.... Yup, You want 5 star funds that're down 10% YTD? Got a handfull available @ Morningstar......goin' DOWN!!!

http://www.sfgate.com/cgi-bin/article.c ... mp;sc=1000

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.sfgate.com/cgi-bin/article.c ... amp;sc=254

TUESDAY

Mark Manning at RealMoney.com points out that the S&P 500 closed below it's 2002 lows Monday. If you bought the low point after the dotcom crash, you're just went down on that investment. Which, by the way was the high in late '96/early '97. If you bought between early '97 and a week ago, with the exception of the 2002 low, and held "For the long run..."you're REALLY hurting. You took a lot of risk, made a lot of money, and lost it. Ya got zero, nada, bupkis. Smooth move; all pain, no gain. But then if you've been reading the COFGBLOG for any length of time and you've been pickin' up what I been layin' down, you know better than to believe in "Buy And Hold For The long Run...One decision stocks and funds, Look at your 401a once a year at the most. That shit's dumber than a box of rocks. Homie does not care to indulge in that recreational pastime.

Pre and Post Bernanke an' Obama speachifying

Bear market bounce and a coupla nice speaches. Do I wanna try and pick up a dollar or two Wed? Will the bounce last long enough to do so? PROLLY NAH. PRETTY WORDS, NO CHANGE IN WHAT'S IMPORTANT.

WEDNESDAY

Ya know, ya can talk grumpy all ya want to about Wall Street and the lying cheats and souless monsters of capitalism and the unbridled greed and stupidity and on and on about all that for as long as you want. But it's American business that is going to put people back to work once this crisis is over and the government is able to stop taxing us and cutting us checks right back. We're gonna have to come to terms with that. Let's have the fit and sturm and drang as necessary and then let's stop the theater. We need some new checks and balances installed and then we need to start the next cycle....

http://www.ritholtz.com/blog/2009/02/tax-rebates/

http://www.ritholtz.com/blog/2009/02/de ... semantics/

http://www.ritholtz.com/blog/2009/02/no ... l-roubini/

Stay tooned.

It Is Now Beginning To Dawn On All And Sundry That The Banks Are Toast. Do We Toss Them And Start Over Or Spend Our Children's Future Trying To Untoast Them. Can Fire Burn Backward?

Saturday, February 14, 2009, 02:18 PM

In general, your target is not to beat the market. It is to beat zero. As I have written for years, the investors who win in this market are the ones who take the least damage.

-- John Mauldin

Chartz and Table Zup @ www.joefacer.com

UPDATED CONSTANTLY....OR NOT.

LOOK FOR THE DAY OF THE WEEK FOR NEW ADDITIONS.

Stay Tooned. Long Weekend an' I'll have something to say toward the end of it. There's a ton o' "stuff" happening. It's all important. But when you get to the end of learning and thinking and planning, the 401a investor in me says "Cash Is King And Think Carefully About The Risk Of Even Thinking About Trying To Catch A Bear Market Rally". The Trader in me sez, "The Trend Is Down And You Can't Imagine Holding A Position Overnight. Roadracing Motorcycles Was An Excellent Preparation For Trading In This Environment."

I love reading Barry Ritholtz' THE BIG PICTURE blog. You can't live this stuff and not have strong opinions. You always know where Barry stands...

from the link below

Time Magazines "25 People To Blame For The Economic Crisis" ...

http://www.ritholtz.com/blog/2009/02/25 ... al-crisis/

A few strange issues with the list: Why is Bernie Madoff here? He is a common thief (perhaps uncommon thief given the amounts he claimed to have stolen) but he had nothing whatsoever to do with the Financial crisis afflicting the global economy. What journalist would add him to the list of causes of the crisis? (Strike that moron from your reading list).

The American Consumers are on the list, but not the irresponsible home buyers? Isnt painting with an overly broad brush ? And Wen Jiabao, the premiere of China? How dare you buy our debt! Its all your fault!

Regular readers of this blog know I think former NAR chief economist David Lereah is a lying jackass, a festering hemorrhoid on the fields of both economics and real estate. But he was merely a lying cheerleader. As much as I detest his syphilitic-addled unfunctional brain, I cannot blame him for what happened.

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.bloomberg.com/apps/news?pid= ... refer=home

I hate the thought that taxpayer money will go to redeem the bad financial decisions of banks and homebuyers who cheerfully made/took loans that were going to take 100% plus of the buyer's income in a matter of two years. I'm uncomfortable with the idea of trying to stand in the way of a flood, or tornado, or negate gravity; Did anyone really think that 10% a year housing appreciation would go on forever and not unwind at some point? Can we borrow enough money to support all the banks and real estate prices at their current level? Will we sell our souls to the treasury bond holders who finance this mess? How much will we have to pay to get somebody to gamble that we can fix this mess without devaluing the dollar? And who will have the money available to by US bonds? Check out the "Time For A Reality Check" link below. Do we saddle everyone who never had a mortgage or just paid off a 30 year mortgage or has 50% equity in their home with years of higher taxes to roll the dice that in the face of a huge economic contraction, the reworked, barely supportable or underwater mortgages don't default again? After mortgaging everyone's future to try prevent the Great Unwind, do we take a second mortgage if it doesn't work? I think we're gonna have our hands full keeping it together so that once the storm is past, we can start the next cycle again. I'm absolutely sure we can't avoid the body of the Great Unwind. I'm in that head space. I hope I'm wrong, but hope ain't no strategy...

I'm not real confident about any of this. The nation needs triage but the politicians ain't gonna tell you that anything is needed beyond first aid. I've got no confidence in the judgement displayed by either administration, so far. Do you?

Why the hell should I be the only one to lose sleep....here's some of what I'm readin'. There's some ticking time bombs in here......

http://www.investorsinsight.com/blogs/t ... check.aspx

http://www.theatlantic.com/doc/print/20 ... -geography

http://www.reuters.com/article/GCA-auto ... 0G20090213

http://www.telegraph.co.uk/finance/comm ... tdown.html

http://www.telegraph.co.uk/finance/econ ... l-out.html

http://www.telegraph.co.uk/finance/comm ... tdown.html

http://www.nytimes.com/2009/02/15/books ... wanted=all

http://www.economist.com/finance/displa ... d=13110352

http://www.reuters.com/article/innovati ... Q120090214

http://blogs.reuters.com/great-debate/2 ... ank-on-it/

http://www.economist.com/specialreports ... d=13063298

http://www.ft.com/cms/s/2/45a7ebca-f712 ... fd2ac.html

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.bloomberg.com/apps/news?pid= ... refer=home

I can't figure out how to invest in this market and it sure seems like no one else can either. Until something changes, the 401a is gonna stay as per the tablez on my website. Nothing ventured everything safe.

TUESDAY

YA WANNA KNOW WHY TODAY LEFT THE MARKET A SMOKING PILE OF SLAG? READ THE LINKS ABOVE!

The market will lift permanently (longer than a day at a time) when things stop getting worse and we can see across the valley to the other side. Until then, we're just looking for a good washout of all the sellers and just a little visibility or some kinda short term relief so we can at least bounce and relieve some short term WAY oversold pressure. It doesn't seem to be happening. HANG ON!!!!!

I'm outa the MET Life GIC as of months ago. It's the highest returning option we have in the 401a and it hurts to be out. But the non-diversified single corporation event risk is huge. MET going the way of Bear Stearns or Lehman Bros is unimaginable. I can't see the the government not keeping them afloat with borrowed taxpayer money. The odds may be in MET's favor overall. But I'm not willing to risk the likely taxpayer money giveaway AND unlikely risk of a GIC default or discount.

http://www.bloomberg.com/apps/news?pid= ... refer=home

And Bill King (The King Report http://www.mramseyking.com/thekingreport.html) commented as follows: A cure should have something to do with the diagnosis. The classic argument for fiscal stimulus presumes that the central cause of our current economic problems is this: We, the people and our government, are not doing nearly enough borrowing and spending on consumer goods. The government must step in to force us all to borrow and spend more. This diagnosis is tragically comic once said aloud.

THURSDAY

LOOK FOR THE INSURERS TO BE THE NEXT SHOE TO FALL....

I GOT A DOLLAR OR TWO IN THE GIC, NO MORE, AND

I'M THINKIN' ABOUT A POLICY LOAN ON MY LIFE INSURANCE. THAT'S A LOT OF SINGLE COMPANY RISK. WHO'S BIG ENOUGH TO INSURE THE INSURERS AND HOW SURE ARE YOU THAT THEY WILL PAY YOU OFF IF THEY GO BELLY UP?

I Moved Some 401a Money Around. When You're Not Happy With Any Of The Choices, How Can You Be Happy With The Decision?

Friday, February 6, 2009, 05:51 PM

The long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is past the ocean is flat again.

John Maynard Keynes

UPDATED CONSTANTLY....OR NOT.

LOOK FOR THE DAY OF THE WEEK FOR NEW ADDITIONS.

I'M INCAPABLE OF NOT EDITING AND REWRITING WHAT'S ALREADY POSTED IF I THINK I CAN SAY IT BETTER. SO IT GOES...

Chartz and Table Zup on www.joefacer.com

I'll get back witcha Saturday (it's Friday night) about my choices and why I moved some money even though I didn't think much of where it was to start with and where it ended up. The 401a site ain't updated and I gotta go....

Friday, (it's Saturday morning) I went off to the GAMH for the first time in a decade or so. Where I had seen Freddie Hubbard, Chick Correa, Jack DeJohnette, Brownie Terry and Sonnie McGhee, David Bromberg, Bobby "Blue" Bland, Tania Marie, Larry Coryell, Bob Segar, Buddy Rich, Billy Cobham, Pat Methany, and Maynard Ferguson, the ownership and management is now from "Slim's" and very much SOMA. Slim's is aka Boz Skaggs'. Culture shock. I saw Still Time, Kapakahi, and Forest Day. Gonna have to stop listening to my 8 tracks and check out what's happenin' in the here and now. There is some interesting music bein' made someplace other than the past.

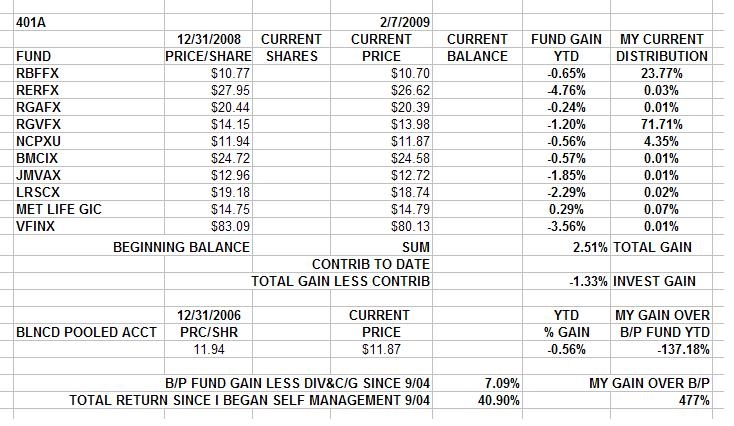

Check out the tablez below. Before and after. This is very likely to change Monday. Or not.

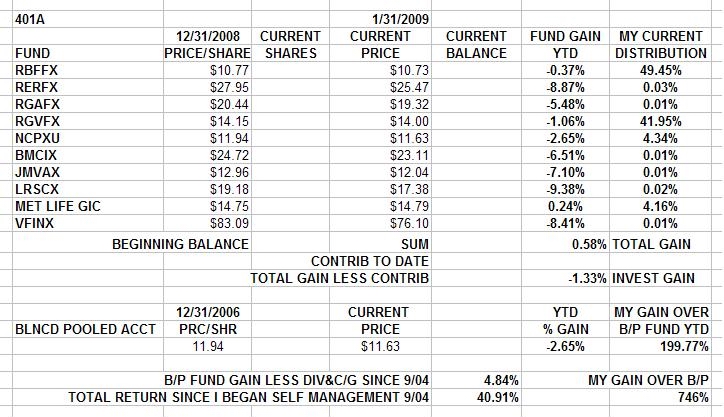

Here's what led to the distribution among funds as of 1/31.....

Starting back in '07, stocks, represented by the S&P 500 Fund VFINX, started to crater. By Spring I had given up on stocks and gone all in to the Met Life GIC/Stable Value Fund. The promised return was above what the bond funds (RGVFX & RBFFX) were paying and MET Life was not Lehman Bros or Bear Stearns. That worked well until late in the Fall (Oct 08) when suddenly things went critical. Check out MET on the chart. The only thing that stands behind the GIC/SVF is MET's promise to return all of the money invested in the fund plus guaranteed interest. Met's assets and worth back up that promise and the stock price is a measure of the confidence in that ability. The market was rendering a judgement on MET's value and undercutting their ability to pay and I hadda respect that. So in the second week of October I went all in to the Am Funds Gov Securities Fund (RGVFX), strictly for safety. I got more than that... Check this out...

About two weeks after I got nervous, everybody else did and piled in after me, bidding up the price of bonds with Fed backing to below zero yield. Who bids up bonds to where they get less back than what they paid? Someone who holds checks for millions of dollars from moving money around and, given the current state of affairs, probably to meet redemptions. Someone who is afraid to give it to a broker or bank or hold a check from a broker or bank. They want/need cash on demand, no excuses. Anybody who was there first like I was, get the bonds he just bought into bid higher. I made up the losses from hanging around for 3 or 4 months in stocks in a coupla weeks of holdin' bonds. That trade started to unwind after Christmas. I wanted to keep most of what I made, so once I was sure of the trend, I moved some money to the AM Fundz general bond fund. I figured that with the new administration on the way and the debt market starting to show the very first signs of thawing, the RGVFX fund would continue to decline in yield and the corporate fund would start to bounce back. That left me with a RGVEX/RBFFX distribution of 'roun' 40%/50% for most of January.

Here's why I changed that Friday and have my money where the table above sez I do.

The markets are feeling queasy about the first days of the Obama administration. Three nominations to major posts with tax troubles and two withdrawn. If Geithner had been a later nomination, he'da gone down too. Too much wafflin' and back an' forth on the bank plan and a growing realization that too much time and money were wasted trying to get a clue and that the delay has made the problem REAL serious. There's a growing realization that we've borrowed and spent ourselves into oblivion and as much as we regret that the party has come to an end, we can't borrow more and relight the ashes. Things are worse than you think. Much worse. The Economic Stimulus package is gonna be hugely expensive and pretty ineffective. The numbers aren't there and there will prolly be at least one and maybe two more ES packages within the next 18 months. Earnings reports have been gawdawful and guidance for next quarter looks REALLY bad. Stocks have been going up but future earnings will be worse, so I don't trust that move. I think Geithner is from the same crowd and mindset (Hank Paulson) that figured that raiding the Treasury and exchanging trash for cash to prop up his contemporaries was an answer to the current debacle. So I want to position myself for a "sell the news" reaction sometime this upcoming week. I would prefer to miss a week or two of the big turn up if I'm totally out of touch as the price of avoiding a possible falling to new lows if I'm right.

What to do? What I did Friday.

Forget the MET Life GIC/SV for now. They look to be the strongest of the big life insurers, but... Put all my money in the hands of ONE company? With no explicit federal backup or something like the FDIC or SPIC? What kinda smart is that? Things gotta work and work out for a while before I trust.

RBFFX?

16% Government bonds

25% mortgage "bonds"

36% corporate bonds

16% foreign bonds

Money here is at risk.... But. One sixth of the fund is government or agency bonds. Can't do better than that. Thirty six percent is various corporate bonds. I can buy them at roughly a 20% discount to last year. And there is cash flow out of these. Dividends are suspended to keep paying bond coupons. I'm down wid dat. If things stop getting worse, we'll turn the corner. They don't have to get better. Once they stop deteriorating, investors will look to the future and bid these back up. Mortgage bonds? We'll see. I'm still paying my mortgage. I did real well in the 80's with bonds. We'll see... Cash flow for now and a possible stock like appreciation once things turn. If things go all Armageddonly, money in a bond fund will be one of my minor problems. Roll the dice.

RGVFX?

48% Gov paper

43% mortgages

I WANT AN ALL TREASURY FUND!!!! But this is the best I can do for now. Half federal paper and hopefully agency insured mortgages.

If the facts change, I'll change my allocationz. This is where I'm at tonight....

This week will be a circus/bar fight/three wolverines in a dryer. I expect to absorb a lot of info and maybe act on it. Or not. Stay tooned....

http://www.markfiore.com/wall_street_executive_air_0

http://www.ritholtz.com/blog/2009/02/jo ... ecessions/

http://www.ritholtz.com/blog/2009/02/th ... ng-crisis/

http://www.ritholtz.com/blog/2009/02/mo ... s-of-rmbs/

http://www.ritholtz.com/blog/2009/02/la ... e-changes/

http://www.msnbc.msn.com/id/29084713/

http://www.newsweek.com/id/183718

http://www.ritholtz.com/blog/2009/02/wi ... y-recover/

http://www.ritholtz.com/blog/2009/02/mo ... s-of-rmbs/

http://www.bloomberg.com/apps/news?pid= ... dj5yq_WnDI

http://www.economist.com/displaystory.c ... d=13057265

http://www.reuters.com/article/ousiv/id ... CQ20090207

http://www.nytimes.com/2009/02/07/busin ... ARKETWATCH

http://www.slate.com/id/2210619/

http://www.nytimes.com/2009/02/08/business/08split.html

http://www.ritholtz.com/blog/2009/02/st ... s-on-fire/

http://www.ritholtz.com/blog/2009/02/it ... that-hard/

http://www.ritholtz.com/blog/2009/02/%E ... n-january/

Monday

http://www.bloomberg.com/apps/news?pid= ... refer=home

http://www.ritholtz.com/blog/2009/02/do ... g-america/

http://www.washingtonpost.com/wp-dyn/co ... 02153.html

http://www.washingtonpost.com/wp-dyn/co ... id=artslot

http://www.washingtonpost.com/wp-srv/na ... ble/video/

http://www.washingtonpost.com/wp-dyn/co ... ml?sub=new

http://www.ritholtz.com/blog/2009/02/mr ... the-truth/

http://online.wsj.com/article/SB123420518851764681.html

Back to the planned US rescue packages, and specifically Bill Kings comments: The main problem plaguing the US economy is too much debt has been accumulated on gratuitous spending and the papering over of declining US living standards. Solons espouse a monstrous surge in debt to fund even more consumer spending. The toxin is not the cure. Inducements to save and invest in production are the remedy. But the welfare state and its ruling class are trying a last grandiose socialist [Keynesian] binge in the hope of salvaging their realm.

By Prieur du Plessis - February 8th, 2009

http://www.ritholtz.com/blog/2009/02/wo ... se-282009/